This online briefing is the fourth in InfluenceMap’s regular series expanding on recent corporate engagement with global methane policy captured on the Methane Platform.

This briefing spotlights the resurgence in oil and gas sector advocacy against the EU Methane Regulation. It then covers the strategies that US-based industry associations are employing to repeal the US federal Waste Emissions Charge on methane emissions from oil and gas operations, and provides a state of play on advocacy concerning other US methane regulations.

Together, these updates indicate an international effort by oil and gas interests in 2025 to gut governments' ability to regulate methane from the energy sector, pushing hard for deregulation in the US while leveraging the pressure of trade talks to encourage a race to the bottom for EU imports. Yet for industries and countries that continue to rely on fossil gas, strong regulatory measures for methane abatement along the oil and gas supply chain remain essential to achieving international climate targets.

Energy companies and industry associations in the EU and US are emphasizing concerns around European energy security in a push to stall and dilute measures in the EU Methane Regulation for the energy sector. Capitalizing on EU negotiations to secure long-term fossil gas purchase agreements to replace Russian gas, the European oil and gas industry — led by Eurogas and the International Association of Oil and Gas Producers (IOGP) — is advocating to delay and undermine the regulation’s measuring, reporting, and verification (MRV) requirements for importers of energy products. IOGP is also calling for the simplification of the methane leak detection and repair (LDAR) obligations.

Additional legislation is now required to fully repeal the Waste Emissions Charge (methane fee) in the Inflation Reduction Act after the Trump Administration’s initial rollback. Groups such as the American Petroleum Institute (API), American Exploration and Production Council (AXPC), and Independent Petroleum Association of America (IPAA) have already begun advocating in favor of this. These groups were also at the forefront of opposition to the fee in initial consultations under the IRA.

In contrast to its staunch opposition to the methane fee, industry’s views on the US Environmental Protection Agency’s OOOOb/OOOOc methane emissions standards and Subpart W reporting rule vary. Rather than pushing to revoke the rules, many entities have instead advocated to weaken them as part of efforts to maintain a degree of alignment with the EU’s methane regulation energy import standards and secure access to European markets, which could be jeopardized if the agency fully repealed them.

In May 2025, the International Energy Agency (IEA) updated its Global Methane Tracker, from which some key findings are summarized below:

Close to one-third of anthropogenic global methane emissions can be attributed to the fossil fuel industry, and energy-related methane emissions do not appear to have peaked yet. Abatement pledges cover 80% of estimated methane emissions from global oil and gas production, however, implementation remains weak.

While the agriculture and waste sectors are major methane emitters, methane mitigation from fossil fuel production offers the greatest potential for immediate reductions. According to IEA scenarios, deploying targeted methane mitigation solutions in the energy sector would prevent a rise of roughly 0.1 °C in global temperatures by 2050. These include addressing leaks and ending routine venting and flaring, which could not only avoid warming and reduce costs but also alleviate supply-demand pressures on the market using captured fossil gas volumes.

EU and US oil and gas interests have increasingly lobbied for weakened measures under the EU's methane rule. Citing concerns over impacts on EU energy security and competitiveness, companies and associations are pushing for delays or adjustments to requirements coming into force in 2025, especially for importers.

The EU Methane Regulation for the energy sector was adopted in August 2024, entering into force incrementally over the coming years, with all requirements scheduled to apply by 2030. Various leak detection and repair (LDAR) requirements, as well as measurement, reporting, and verification (MRV) obligations, will begin to apply in 2025 for both operators of EU-based oil, gas, and coal facilities and importers placing energy products originating from third countries on the EU market.

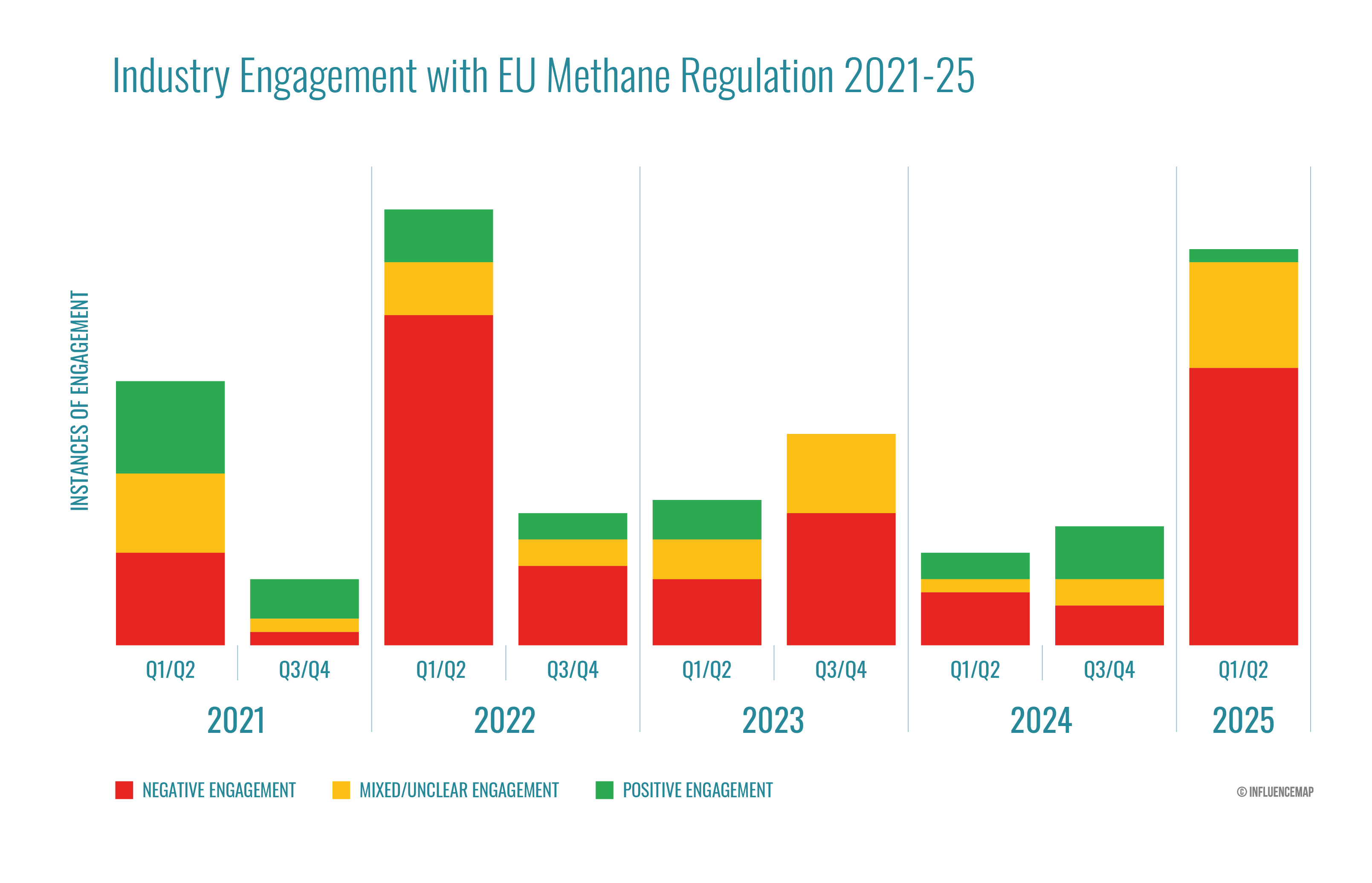

In 2025, InfluenceMap detected an uptick in industry advocacy against the file, coinciding with the EU strategy to phase out Russian fuel imports by 2027. Companies and industry associations are calling for less stringent measures, highlighting the regulation’s consequences for importers and pushing the narrative that this consequently poses a risk to the EU’s energy security. The graphic below illustrates all industry engagement with the policy identified by the LobbyMap database since its proposal. The spike in negative advocacy in 2025 is comparable to levels of engagement during the initial consultation period in February–May 2021 and during the feedback period from December 2021–April 2022.

Under the rule, energy importers need to prove that their products comply with EU standards for methane MRV and emissions intensity. From May 2025, fossil fuel importers are required to provide basic data on certain methane emissions monitoring and mitigation measures, which will be published in an EU database with country performance profiles from 2026. Reporting templates will be established by an implementing act, until which operators are expected to follow Oil & Gas Methane Partnership (OGMP) 2.0 reporting guidance. From 2027, demonstrating compliance with EU-equivalent MRV standards for methane emissions at the point of production will be mandatory for all contracts signed between foreign suppliers and European buyers after August 2024. Besides producer-level equivalence, the EU will also develop a framework for establishing equivalence at the country level with third nations.

Industry pressure on EU policymakers to weaken reporting requirements and accelerate the establishment of regulatory equivalency with third nations — including the US, where methane regulations are at risk of significant revision — could undermine the regulation’s ambition of reducing emissions along the supply chain:

In a February 2025 interview with POLITICO, the European managing director of the International Association of Oil and Gas Producers (IOGP) suggested that the EU methane regulation “jeopardizes” a deal with Trump to secure US liquefied natural gas (LNG) and indicated industry’s renewed efforts to “reopen” the file.

In March 2025, Eurogas published a position paper of recommendations for the regulation, emphasizing concerns over its impact on EU competitiveness and security of supply as the bloc seeks to replace Russian gas imports. The statement advocated to delay the Chapter 5 MRV obligations for importers until relevant implementing rules are in place, or to add a grace period for penalties. It also recommended a “pragmatic” approach to determining country-level equivalence and proposed a book-and-claim system for tracing the origin of fossil gas imports. This would allow producers to buy certificates for compliant imported volumes and claim their environmental attributes, potentially providing inaccurate attributions of MRV practices and methane intensities and eliminating incentives to reduce emissions. The group reiterated these points to the media later that month. In April, Eurogas objected to the reporting requirement in an interview with Euractiv and advocated for US LNG to automatically comply with the regulation in an interview with POLITICO.

In April 2025, a joint letter addressed to EU Commission officials from 19 US and EU energy entities highlighted the “significant challenges” the regulation creates for the “security of the EU’s gas supply, particularly as the EU seeks to ensure affordability and … replace Russian gas imports.” It also advocated to delay the Chapter 5 MRV equivalence and the methane intensity reporting obligations until implementing legislation is in place, and requested a grace period in the meantime, including that contracts signed during the period are protected from the risk of penalties. Signatories included BP, ConocoPhillips, Engie, Eni, Equinor, Eurogas, Naturgy, Repsol, and Uniper.

In May 2024 meeting correspondence with the cabinet of EU Commissioner Maroš Šefčovič, accessed by freedom of information request, LNG company Cheniere Energy characterized the MRV requirements for importers as "unworkable" for the US LNG supply chain and called EU-US equivalency “critical.”

In November 2024, Reuters reported on a letter to EU officials signed by trade groups, including the US Chamber of Commerce and American Petroleum Institute (API), flagging concerns about the requirements and the impact on EU security of supply.

In a March 2025 letter to the US Trade Representative, the US Chamber reiterated these concerns and urged the US to initiate the formal process with the EU for determining MRV equivalence.

Concurrently, the EU is considering amendments to several sustainability reporting laws through a collection of legislative proposals known as the “Omnibus package." Included in the Omnibus are proposed changes to the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD), and the EU Taxonomy. As timelines line up with the first of the methane regulation’s requirements, the European branch of the international industry association IOGP has consistently advocated to add the EU Methane Regulation within the scope of the Omnibus:

In a list of recommendations for the Omnibus proposal from January 2025, IOGP Europe advocated to remove the leak detection and repair obligations for equipment below a certain methane repair threshold, stressing costs and the risk of diverting resources from “more impactful” leaks.

In a February 2025 position statement, IOGP Europe emphasized concerns that the EU Methane Regulation could jeopardize the EU’s energy security and urged the Commission to include it in the Omnibus “as soon as possible” to address technical implementation challenges and set “workable” timelines for compliance.

In a separate February 2025 publication, IOGP Europe suggested that simplifying the regulation via the Omnibus would help drive European industrial competitiveness.

While the European Commission has not included the methane regulation in the package, this demonstrates how corporate groups are taking advantage of the Omnibus and wider simplification trend to push to weaken climate policy.

The Commission is also required to adopt secondary legislation for the implementation of technical aspects of the methane regulation. According to the Commission’s website, feedback is upcoming for the Delegated Acts regulating the minimum methane detection limits and techniques and the emissions reporting templates for operators. InfluenceMap has already uncovered direct engagement with policymakers by IOGP on the former, with both acts likely to be subject to significant further lobbying. Weak Delegated Acts increase the risk that the global oil and gas supply chain will fail to reduce its methane emissions in line with climate targets. InfluenceMap will assess industry engagement once the consultation responses have been released.

The Trump administration has delivered on its promise to repeal the federal charge on excess methane emissions from oil and gas operations, reflecting industry demands.

In February 2025, the US Congress voted to repeal the regulation implementing the Waste Emissions Charge (methane fee) enacted in November 2024 under the Inflation Reduction Act (IRA). In 2025, the Environmental Protection Agency (EPA) was due to begin calculating charges based on 2024 emissions data for the first year of penalties under the fee. However, the US Senate and House passed a joint Congressional Review Act resolution to repeal the rule, which was signed into law by President Trump on March 14. This follows years of intense, targeted opposition from industry, including at the following key policy moments in 2025.

In January 2025, as Trump’s second presidential transition was underway, industry targeted their messaging at the new Congress and other government staff assuming office:

The American Exploration and Production Council (AXPC) included repealing the methane fee in a letter of recommendations for the 119th Congress and a separate letter to the acting administrator of the EPA. The API released an updated policy memo to the EPA, which asks the agency to permanently repeal the fee, including the enabling statute to prevent potential future iterations of the policy.

Two Texas Republicans introduced the Natural Gas Tax Repeal Act in their respective chambers of Congress, which is designed to overturn the methane fee following the standard repeal process:

API, AXPC, and the Independent Petroleum Association of America (IPAA) reportedly endorsed Senator Ted Cruz’s (R-TX) reintroduction of the bill in the Senate. Consumer Energy Alliance (CEA) also supported Cruz’s bill in social media posts. Meanwhile, API and AXPC are quoted as supporting Congressman August Pfluger’s (TX-11) introduction of an identical bill into the House.

In February 2025, US policymakers began implementing the Congressional Review Act (CRA). It provides an expedited procedure for nullifying recent federal regulations — requiring only a simple-majority vote in both chambers and presidential approval — and blocks the implementation of a “substantially similar” policy in the future unless authorized by a subsequent law. Trade groups have pivoted to endorse the use of the bicameral CRA at every step of the process:

Industry groups expressed support for the introduction, House and Senate passage, and presidential signing of the CRA through press releases and social media. This includes the IPAA, AXPC, API, and National Association of Manufacturers (NAM).

API opposed the fee in testimony at a House Committee on Energy and Commerce hearing on regulations hampering the oil and gas industry. AXPC also submitted a letter to the record reiterating their advocacy to repeal the fee.

The API, US Chamber of Commerce, and National Federation of Independent Business (NFIB) submitted letters to the Congressional Record all advocating to use the CRA to overturn the fee, citing impacts to energy production.

The CRA resolution does not eliminate the underlying statute in the Inflation Reduction Act that permits the application of such a fee, meaning that the legislative grounds to charge oil and gas sources for relevant methane emissions remain intact. If the fee were to remain codified, it could give future administrations the authority to implement a fee on methane emissions from the energy sector. However, members of Congress intend to use the upcoming budget reconciliation package to completely overturn the Waste Emissions Charge and other IRA provisions, according to media reports. In March 2025, the IPAA and AXPC published updated policy briefs on their websites, advocating to scrap the statutory mandate for the fee. Ongoing analysis of recent corporate engagement with this process is available on the Inflation Reduction Act policy page on InfluenceMap’s US platform.

The US Administration’s deregulatory approach could complicate potential equivalence agreements with other regions’ methane import standards. Unlike coordinated messaging against the methane fee, mixed positions from industry around the potential rollback of further federal US methane rules suggest concerns over foreign market access.

Among a swathe of other policies, the EPA announced on March 12 that the agency is reconsidering both the Biden administration’s New Source Performance Standard OOOOb and Emissions Guidelines OOOOc methane regulations (OOOOb/c), and the Subpart W reporting revisions for the oil and gas industry. The finalized OOOOb/c rules, published in December 2023, establish methane emissions standards for new and existing oil and gas facilities, including leak detection and repair measures for methane emissions from wells and restrictions on routine venting and flaring. The Subpart W reporting revisions, finalized in May 2024, expand the scope and accuracy of methane emissions reporting from the oil and gas industry by requiring empirical data from direct site-specific measurement and adding a category for large emission events.

The agency’s action aligns with the two-pronged approach pushed by industry association policy recommendations in the lead up to and following the November 2024 presidential election, which suggested revoking the methane fee and modifying the regulations. Further coverage of this advocacy can be found in InfluenceMap’s January 2025 methane bulletin.

Corporate engagement in 2025 on the methane regulations has been comparatively scarce and demonstrated a mixture of unclear and unsupportive positions:

In its January 2025 policy memo to the EPA, API advocated to “finalize the current reconsideration methane rule consistent with industry recommendations,” including numerous revisions that would weaken specific technical elements of both the OOOOb/c and Subpart W rules.

In a February 2025 letter to Congress, AXPC appeared to support the methane regulations and revisions to the reporting rules with exceptions, without expanding further on desired amendments. In a similar letter to a House Committee hearing, the group reiterated asks to amend both the rule and reporting revisions through the administrative process with no further details.

In March 2025, the IPAA issued a press release in response to the EPA’s reconsideration announcement, advocating for amendments to both policies relating to costs and small wells.

In a March 2025 policy brief, AXPC claimed to be broadly supportive of many of the requirements for the OOOOb/c rule while stating that there are “significant flaws” for which the group is “seeking targeted improvements.”

A lack of clear, consistent positions from oil and gas entities may indicate the sector’s concern that deregulating methane in the US could restrict US gas producers' access to European markets. Emissions reduction and reporting requirements in the EU Methane Regulation are enforced on the entire supply chain. Although the EU has not yet determined how other countries’ regulations could be deemed equivalent to its own, the Biden administration was reportedly in talks with the EU in December 2024 to establish regulatory equivalency between the two nations to safeguard LNG trade flows. In the event of a significant overhaul of the US methane standards and reporting rule, US oil and gas producers could struggle to prove that the oil and fossil gas they produce meet the as-yet-undefined methane intensity thresholds along with the monitoring, reporting and verification requirements of the EU Methane Regulation. Non-compliance could complicate long-term gas purchasing agreements and incur fees on energy imports to the EU.