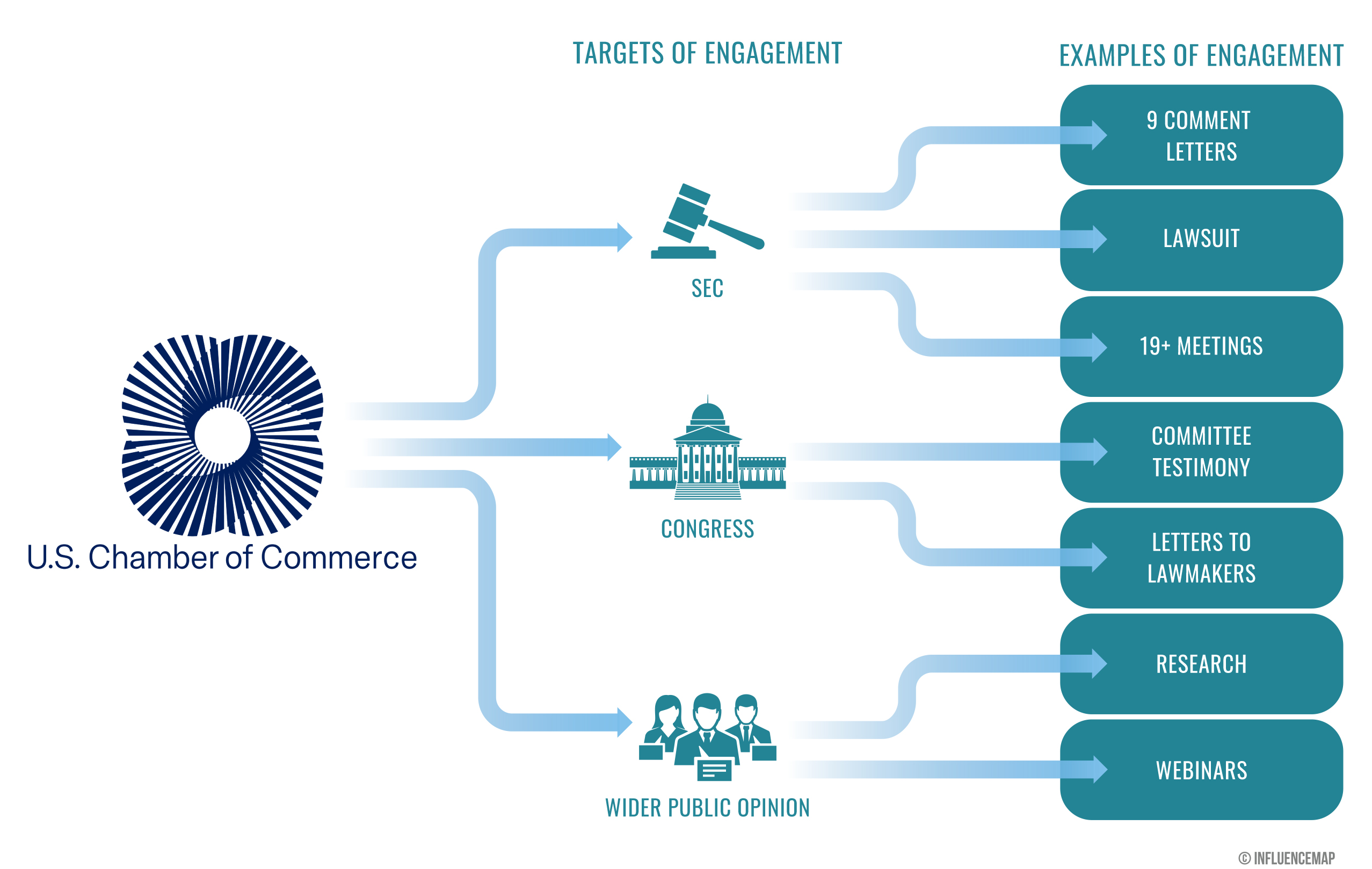

The Chamber has, in its own words, been “at the forefront of fighting” the SEC’s climate disclosure rule. Years before the rule’s introduction the Chamber was opposing the need for regulated corporate climate disclosure: in a 2019 press release the Chamber asserted that “Congress and the SEC should reject proposals for one-size-fits all disclosure mandates.” After the rule was proposed in 2022, the Chamber wrote to the Commission in opposition to the proposal, suggesting it exceeded statutory authority and raised “serious constitutional questions” by “violating the First Amendment.” The Chamber submitted several supplemental comment letters on the proposal, each bringing forth an additional explanation for its opposition to the rulemaking. The Chamber argued that the “major questions doctrine” outlined by the Supreme Court in West Virginia v. EPA “confirms the Commission’s lack of statutory authority” to bring the rules. It asserted that the assumption that environmental considerations are important to investment decisions “is not accurate,” and cautioned the Commission against factoring California disclosure laws into its own decision making, stating that the laws “suffer serious legal flaws” and “burden interstate and foreign commerce.”

In addition to comment letters, per the SEC’s disclosures the Chamber met with the Commission 19 times after the rules were proposed. Representatives from the Chamber, in congressional testimony, urged lawmakers to “exercise oversight of financial regulators” requiring climate disclosure and supported legislation that would limit the SEC’s authority to mandate climate disclosure. The Chamber has hosted webinars and produced research to assert that the SEC’s rules “impose costs” and are not necessary given the widespread nature of voluntary corporate ESG disclosure. Figure 1 shows the different targets of and avenues for the Chamber’s opposition.

The Chamber’s strong opposition to the SEC’s rules is at odds with the positions of many of its members, both financial and non-financial companies. Additionally, the Chamber’s decision to pursue litigation even after the final rule was significantly weakened calls into question the Chamber’s stated commitment to “work constructively with the SEC to develop clear and workable rules for climate disclosures.”

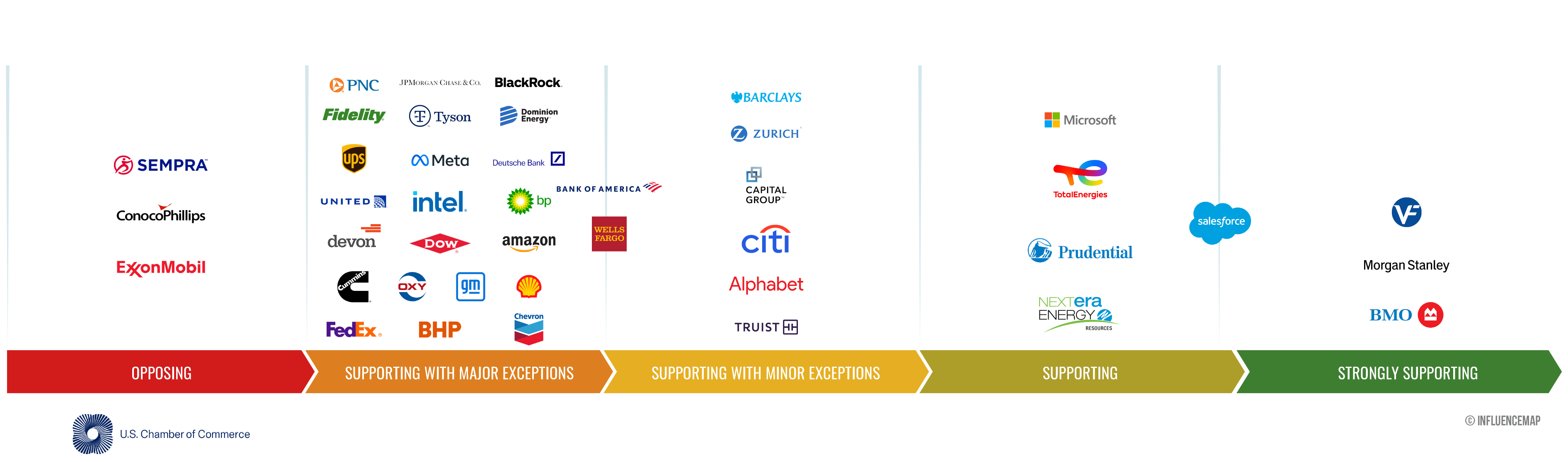

The graphic below shows the misalignment between the Chamber’s position on climate disclosure policies and the positions of some of its members. Members’ positions along the spectrum are determined by their stances on climate disclosure policies at the SEC, in California, and in the EU (Corporate Sustainability Reporting Directive (CSRD)). Where members have not engaged on one or more of these policies, their position is only determined by the policy on which they have engaged. In addition to its opposition to SEC disclosure rules, the Chamber brought a lawsuit against the California climate disclosure laws and asserted that it was trying to “ward off” the EU rules from taking effect.

The table below highlights comments about the SEC’s climate disclosure rule from select members of the US Chamber. These supportive comments demonstrate examples of members’ own positions diverging from the Chamber’s strong opposition to the rule.

| Entity | Comments on SEC Climate Disclosure Rule |

|---|---|

| Bank of Montreal | “We therefore support the SEC's Proposed Rule requiring all public companies to file climate-related financial information with the Commission including TCFD-aligned mandatory Scope 1, Scope 2, and material Scope 3 reporting.” (Comment to SEC, June 2022) |

| Capital Group | “We commend the Commission for its engagement in this important and complicated matter, and for what we believe is, on the whole, a balanced proposal … While some investors believe it is premature to mandate Scope 3 GHG emissions disclosure, and we recognize the challenges involved in measuring the same, we strongly believe – as described more fully below – that larger companies should disclose this information to the extent material,” (Comment to SEC, June 2022) |

| Salesforce | “We sorely need a standard approach for companies to produce climate information that investors and markets need. That is what the U.S. Securities and Exchange Commission (SEC) is working to create. … Now, it’s time for corporate America to vocally support a regulatory framework and close a critical gap between investment decisions and key insights into a company’s exposure to climate-related risks and positioning to succeed in the transition.” (Insight, June 2022) |

Several commenters objected to the Scope 3 disclosure requirements in the March 2022 proposed rule. For example, Devon Energy wrote “we request the SEC omit any requirements to disclose Scope 3 emissions,” BlackRock suggested the Commission allow “material Scope 3 disclosures to be furnished in the New Form on a “comply or explain” basis, which allows issuers to either disclose material Scope 3 emissions or explain why certain emissions categories are not relevant to the issuer or not subject to reasonable estimation,” and Uber wrote “Scope 3 emissions disclosure requirement should in all cases be limited to the Scope 3 emissions categories that are themselves material for a particular company, irrespective of whether a company has set targets or goals in relation to Scope 3 emissions in their totality.”

The Chamber’s decision to pursue litigation even after the SEC removed Scope 3 disclosure requirements from the final rule calls into question the Chamber’s stated commitment to work “constructively” with the SEC to “develop clear and workable rules” around climate disclosure.