This is the fifth online briefing in InfluenceMap’s regular series collating recent corporate engagement with global methane policy, captured on the Methane Platform.

This briefing draws on data and analysis from InfluenceMap’s LobbyMap platform to highlight recent corporate engagement with methane policy globally, with a focus on activity ahead of COP30:

Major companies and industry associations in the meat and dairy sector, several of which are likely planning to attend COP30, have been promoting an alternative approach to measuring the climate impact of short-lived greenhouse gases such as methane since at least 2020. The GWP* metric is not formally accepted by the Intergovernmental Panel on Climate Change (IPCC) and may constitute another prong in the narrative playbook pushed by the agricultural industry to downplay the climate impact of methane emissions from the sector.

Multinational food corporation Danone joined an NGO in calling for dairy methane reductions to be prioritized under the EU’s 2025 Vision for Agriculture and Food, establishing best practice for dairy companies by demonstrating science-aligned advocacy on the climate impact of anthropogenic methane and the need to regulate emissions from the sector.

The international implications of the EU Methane Regulation’s measures on fossil fuel imports have prompted concerted transatlantic lobbying from US trade groups such as the American Petroleum Institute, LNG Allies, and Center for LNG. Their campaign aims to delay implementation, lower enforcement standards, and secure regulatory equivalence for US exports despite ongoing methane deregulation in the US. European industry groups have echoed similar demands, pressing for delays and the regulation’s inclusion in the EU’s simplification agenda. Amid this pressure, a coalition of institutional investors has urged EU policymakers to maintain the regulation as adopted.

Meanwhile, under the Trump administration, the US Environmental Protection Agency has taken steps to reduce methane reporting requirements, proposing to delay the obligations for oil and gas companies under the Greenhouse Gas Reporting Program until 2034. With the European Commission seemingly withstanding pressure to weaken the Methane Regulation’s import standard, the US oil and gas sector appears concerned that this delay significantly damages any case for US equivalency with the EU rule.

In October 2025, the EAT-Lancet Commission released an update to its flagship 2019 publication on sustainable food systems. Some new takeaways for methane emissions are summarized below:

Food systems drive five different planetary boundary transgressions, including approximately 30% of total global greenhouse gas (GHG) emissions driving climate change (16–17.7 Gt of CO2-equivalent per year). Around a third of these emissions stem from agriculture, including both livestock and crop production, with animal-sourced food production accounting for the majority of the sector's emissions.

Methane emissions linked to the meat and poultry industry—from both enteric fermentation in ruminant livestock and manure management—account for a large proportion of agricultural emissions. Widespread adoption of a planetary health diet (predominantly plant-based, with moderate inclusion of animal-sourced foods and minimal consumption of added sugars, saturated fats, and salt) could cut non-CO2 GHG emissions such as methane from agriculture by 15% before 2050.

The Commission reported that without a global transformation, food systems will be responsible for breaching the Paris Agreement goal to limit global warming to below 1.5ºC even in the event of a global transition away from fossil fuels.

These findings once again reinforce the significant role that the agricultural sector plays in driving climate change and emitting short-lived climate pollutants such as methane, despite the industry’s efforts to obfuscate its impact in the methane policy debate.

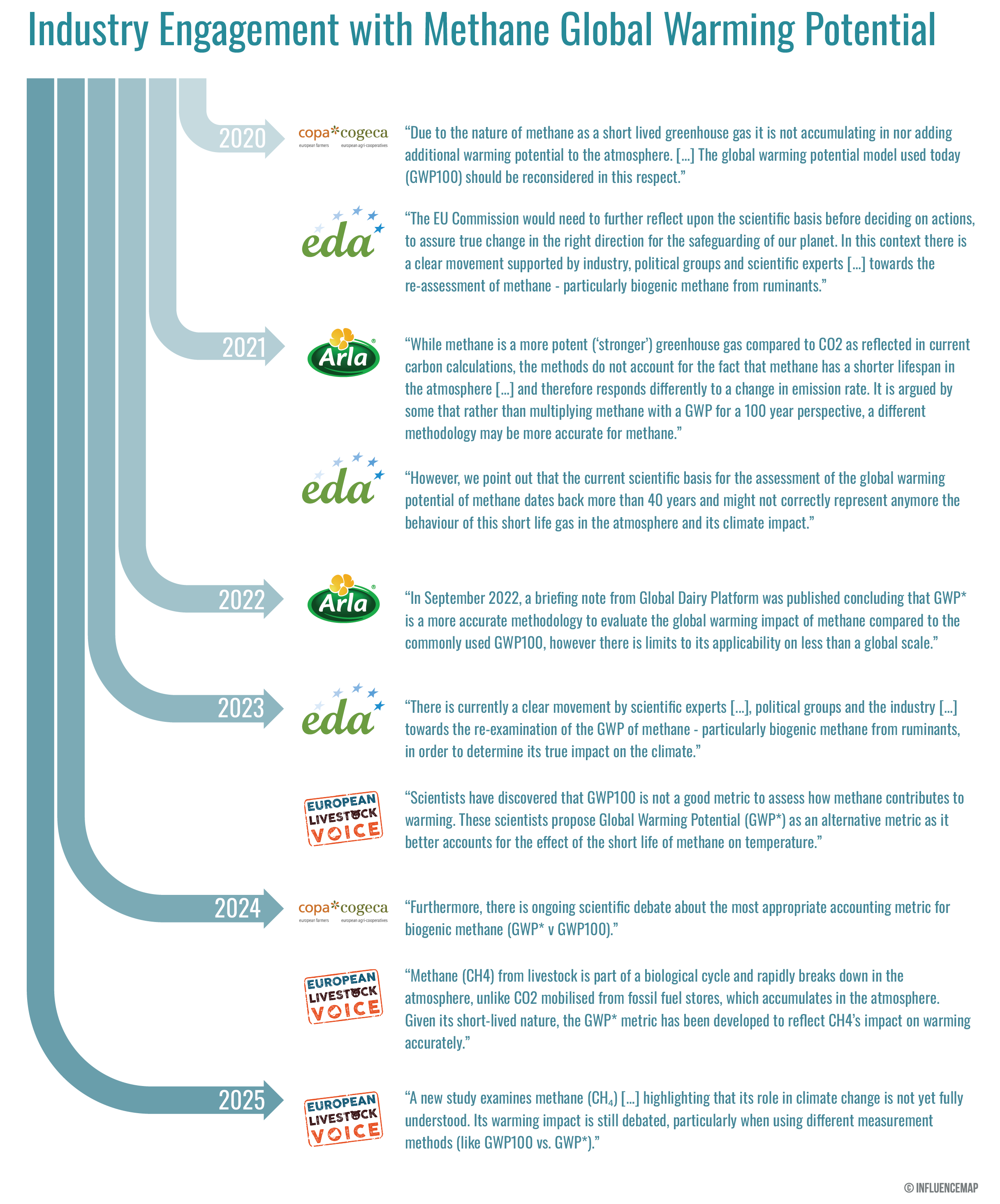

All GHGs have different global warming potentials (GWP), which measure how effectively each gas traps heat in the atmosphere. Ahead of COP30 in Belém, InfluenceMap has reviewed recent agricultural industry communications referencing alternative warming metrics for methane. GWP*, which the IPCC has rejected as an official metric for cross-sectoral methane comparisons, appears to be gaining traction with policymakers.

Developed in research published in 2018, Global Warming Potential* (GWP* or GWP-star) is an alternative approach to measuring the climate impact of short-lived GHGs such as methane. The metric adjusts for historical emissions and the relatively short atmospheric lifetime of methane by focusing on the changes in emissions rates, rather than total emissions values, over any given time horizon. GWP* relates cumulative CO2 emissions to date with the current rate of emission of short-lived climate pollutants such as methane.

GWP* diverges from the traditional GWP100 measure, which standardizes other gases’ atmospheric warming in terms of their CO2-equivalent impact over a 100-year timeframe. The IPCC’s Sixth Assessment Report provides two static values for methane GWP relative to CO2: 29.8 for fossil methane and 27.0 for methane from all non-fossil sources. In other words, one ton of methane emitted by livestock has an equivalent warming impact over 100 years as 27 tons of CO2.

Metric choice can shift the apparent responsibility for warming of different polluting sectors. Using GWP*, a source with a stable rate of methane emissions would appear to cause negligible additional warming (even if those emissions are high), because gas is removed at the same rate as it is replenished. Some scientists have suggested this “no additional warming” framing is misleading, as it masks the dangers of sustaining current levels of atmospheric warming from methane and risks deprioritizing the rapid and deep methane reductions needed to slow the rate of warming and buy time to tackle emissions from other sectors.

GWP* is not currently endorsed by the IPCC, which currently states that it can provide a “useful additional perspective about the effect of cumulative methane emissions.” The IPCC's Sixth Assessment Report reaffirmed GWP100 as the standard for comparability across sectors and gases and rejected the use of GWP* as a replacement for GWP100 in emissions inventories or policy, stating that it “does not capture the contribution to warming that each methane emission makes.” GWP100 is embedded in UNFCCC frameworks, including the Paris Agreement and countries’ Nationally Determined Contributions, as well as other international mechanisms such as emissions trading schemes.

InfluenceMap has identified consistent messaging about GWP over the last five years from key European livestock and dairy organizations, including in direct policy consultations. Messaging on GWP spans a range of positions: from questioning the value of GWP100; to simply noting the relevance of GWP*; to suggesting that GWP* is a more accurate or fair way to account for methane emissions from agriculture, which could be used to argue for a reduced perceived warming impact from the sector.

Industry promotion of GWP* comes in parallel with intensive engagement from the agricultural industry to weaken the case for robust methane policy for the sector. Previous InfluenceMap analysis outlined a two-pronged playbook, by which industry simultaneously minimizes the climate impact of methane emissions from livestock production in a manner that suggests it is a less harmful form of pollution, and pushes the narrative that methane regulations would bring about negative real-world impacts, such as on food security and prices.

The GWP* debate appears to be shaping the methane policy agenda. For example, the government of New Zealand weakened its biogenic methane target in October 2025, including applying the “no additional warming” concept, which seems to reflect GWP* framing. Scientists and NGO groups appear concerned that other governments with large livestock sectors will follow suit, such as Ireland and Uruguay.

It is likely that alternate methane metrics such as GWP* will be promoted at COP30, particularly as several agribusiness actors including Marfrig, JBS, the Brazilian Agribusiness Association, and the European Dairy Association were registered as in-person participants last year. Their participation underscores the need for stakeholders and policymakers at COP30 to be aware of how industry actors have used narratives to reshape the dialogue around agricultural methane emissions.

Danone has joined EDF in calling on the EU to focus on reducing methane emission in the dairy sector.

In February 2025, the EU presented its Vision for Agriculture and Food. The document builds on the conclusions of strategic dialogues, which ran from January to September 2024, that were overshadowed by protests and rising tensions within the farming industry across member states. The dialogues included farmers, NGO groups, and academics, as well as trade associations, some of which InfluenceMap finds to be lobbying negatively on climate policy. Key groups such as Europe’s largest farming union Copa-Cogeca appeared to play a particularly influential role, with multiple representatives in attendance across the plenaries and meeting with Commissioners outside of the dialogue framework to discuss agriculture-related topics throughout the consultation period.

In a joint letter with the Environmental Defense Fund earlier that month, Danone called for the EU's Vision for Agriculture and Food to focus on the reduction of methane emissions in the dairy sector, setting a strong example of ambitious corporate methane policy engagement for agricultural companies:

Danone advocated for EU policymakers to support dairy farmers in reducing methane from dairy, calling for both incentives and policy to enable action without jeopardizing livelihoods.

The statement included a detailed position on the climate science of methane emissions from the agricultural sector, acknowledging methane’s increased potency compared to CO2 and the potential to slow near-term global warming by rapidly reducing methane emissions.

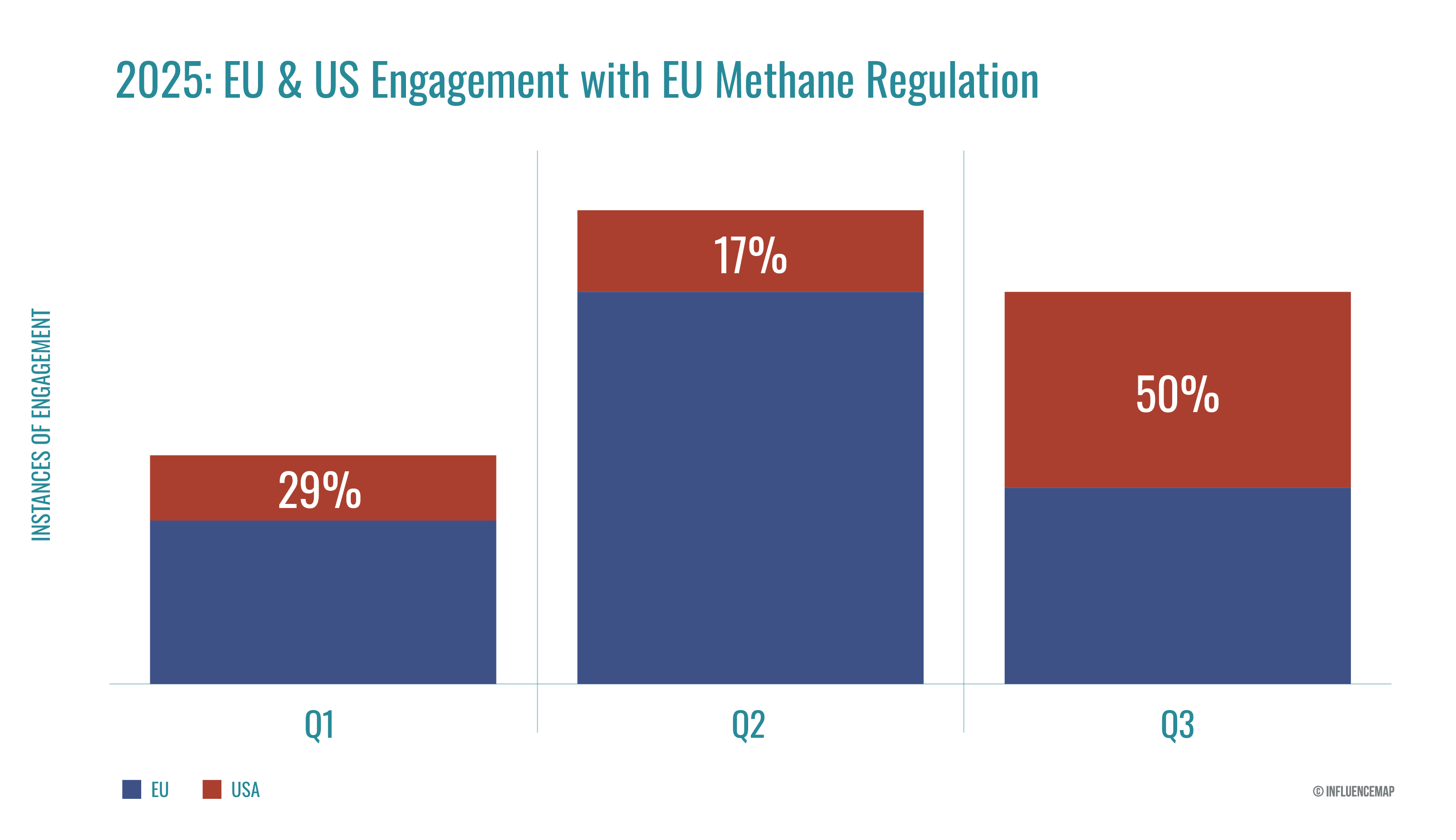

Since InfluenceMap’s previous methane bulletin in June 2025, the global oil and gas industry has continued its campaign against the EU Methane regulation for the energy sector. Companies and trade groups located in the US have intensified efforts to weaken key provisions of the law relating to fossil fuel imports.

In July 2025, following protracted negotiations, the EU and US struck a trade agreement committing the EU to purchasing $250 billion in US energy products over the next three years. Industry has identified the EU Methane Regulation as a potential barrier to LNG flows from the US. Starting in January 2027, the regulation will require producers of oil, fossil gas, and coal to prove that contracts signed from 4 August 2024 onwards are subject to monitoring, reporting and verification (MRV) measures that are equivalent to EU requirements. For contracts finalized before that date, importers “shall undertake all reasonable efforts” to require that their fossil fuels are subject to those same MRV measures.

In a diplomatic trip to Brussels in September, US Energy Secretary Chris Wright and Interior Secretary Doug Burgum asked the bloc to rethink the regulation, stating that it “significantly threaten(s) the ability to implement the trade deal that was agreed to.” Their message echoes mounting pressure from oil and gas companies and industry associations, which has ramped up since the beginning of the year to weaken the implementation of the rule. The following graphic shows the increasing proportion of oppositional advocacy from US-based entities since the start of 2025:

Specific lobbying efforts have sought to weaken the regulation by revising the requirements around measuring, reporting, and verifying methane emissions along the supply chain, or delaying timelines for transparency measures on fossil fuel imports. In addition, certain companies and industry associations have pushed to establish “regulatory equivalence” with the US, under which US imports would automatically comply with EU rules despite the US delaying or dismantling its own methane rules (see section below). Other companies have pushed for reduced penalties for non-compliance at the EU Member State level. Collectively, these asks risk undermining the regulation’s objective of reducing methane emissions along the fossil gas supply chain:

An American Petroleum Institute (API) representative revealed on a podcast in June 2025 that the group pushed for the US to be considered equivalent to the EU, allowing US imports to automatically comply with the rule despite methane deregulation in the country. In an August 2025 media statement, API asserted that the regulation makes it “more difficult for companies to provide the energy that their consumers need” in the wake of Russia’s invasion of Ukraine, stating: “Don’t bite the hand that feeds you.” In a September 2025 statement, API declared that it would continue working with the US administration to push for delayed implementation and “practical” compliance requirements for US energy exports.

In June 2025, the US LNG Association (LNG Allies) President Fred Hutchison characterized the rule as a “trade barrier that needs to be reduced” and reportedly sent a letter to US and EU officials advocating for a trade deal under which US exporters are deemed equivalent under the rule. In July, Hutchison told Politico that the rule was poorly designed, referring to the measures for supply chain transparency. In an August 2025 podcast interview, Hutchison stated that he remained hopeful for an equivalency agreement, but in September, he implied that the only workable solution for US producers and exporters would be for the EU to substantially amend the rule.

In July 2025, 11 Members of US Congress issued a letter to the US Trade Representative Jamieson Greer urging the Trump administration to push back on “discriminatory” EU energy regulations that “threaten American exports and undermine the US-EU energy partnership,” including the methane regulation. The US Chamber of Commerce, API, and American Exploration and Production Council (AXPC) endorsed the letter, with the US Chamber stating that the rule “unfairly discriminates against energy exporters helping Europe phase out its dependence on Russian gas.”

In reporting from July 2025, Center for LNG director Charlie Riedl appeared to express concern that US exporters will be unable to meet the EU’s standards and that compliance challenges have already impeded contracts and investment decisions. He admitted that companies are gambling on the rules being “relaxed” and pointed to different ways to undercut enforcement, such as an equivalency agreement with the US or EU Member States setting negligible penalties. In September 2025, Reidl urged the EU to “at a minimum” delay the start date for the rules and grandfather in any long-term contracts signed before then. Riedl reacted positively to comments later that month from Energy Director General Ditte Juul Jorgensen that the EU would work to implement the regulation “in a way that doesn't constitute an irritant in any way.”

In a statement to S&P Global in September 2025, a representative from EQT stated that it is “impossible” for US operators to be confident they comply with the EU regulation, and that “the needed clarity will not come until the rules are revised to address the realities of the US natural gas value chain.”

European oil and gas entities have also continued their campaign to revise the regulation, reiterating calls for the EU to include it in a simplification Omnibus and recycling narratives relating to energy security and competitiveness:

In June 2025, the European arm of the International Association of Oil and Gas Producers (IOGP Europe) released a position paper emphasizing concerns with specific MRV and leak detection and repair (LDAR) requirements, as well as Chapter 5 obligations for importers.

In July, seven European industry associations including Eurogas, FuelsEurope, IOGP Europe, and the International Gas Union (IGU) published a joint action plan specifically targeting the rules for importers. The document characterized the primary legislation as “unworkable” and advocated to delay both MRV equivalence and methane intensity reporting requirements until implementing guidance is established. It also argued for a grace period on the application of penalties as well as grandfathering of contracts signed during this period.

Eurogas, FuelsEurope, and IOGP Europe sent a joint letter to the EU Energy and Simplification Commissioners in August 2025, urging them to integrate the EU Methane Regulation into the EU simplification agenda. The letter restated that the regulation’s timelines are unworkable for domestic and imported energy, and advocated to delay implementation and reduce non-compliance penalties.

IOGP Europe issued a letter to the EU Competitiveness Council in September 2025 again asking for the EU Methane Regulation to be included in the simplification agenda.

Following the visit from President Trump’s Cabinet, EU energy commissioner Dan Jørgensen confirmed that the bloc will not withdraw the legislation at the behest of the US. However, there remains a risk that the EU could offer concessions regarding the country’s compliance.

In the midst of bilateral industry pressure, investors are pushing back in favor of advocacy to sustain the regulation’s ambition: in an October 1 joint letter, investors including Aegon, Scottish Widows, and Robeco urged the European Commission, Parliament, and Member States to “maintain and implement” the EU Methane Regulation and cautioned against any reopening of the regulation in an omnibus process.

Sustained stakeholder engagement will be necessary to ensure the Commission supports robust implementation of the EU’s methane regulation, particularly as it develops upcoming secondary legislation.

The latest to undergo the Trump Administration’s deregulation agenda is the Greenhouse Gas Reporting Program (GHGRP), including Subpart W segments for reporting methane emissions from petroleum and fossil gas sources. In September 2025, the Environmental Protection Agency (EPA) announced a proposed rule to suspend reporting obligations for Subpart W segments until 2034, characterizing the GHGRP as “burdensome” and creating high regulatory costs for producers with “no material impact on improving human health and the environment”.

The EU has agreed to buy hundreds of billions of dollars in US liquefied fossil gas, but starting in 2027, the bloc will require importers to prove that energy products placed on the European market meet EU standards on methane MRV. Without the GHGRP emissions database to demonstrate compliance, US fossil fuel exports to the EU could face penalties and potentially exclusion from the market. Despite this risk, oil and gas actors have not pushed to retain the reporting rules which they admit could have been used to “patch together a reasonable case on country level equivalency”. Instead, the industry’s strategy appears focused on trying to weaken EU requirements ahead of implementation in 2027 (see section above).

InfluenceMap’s June 2025 Methane Bulletin outlined the fossil fuel industry’s ambiguous reaction to the initial reconsideration announcement. Likely due to the EU Methane Regulation import standard, oil and gas associations sought modifications to reporting rules, but none have explicitly advocated to scrap or delay it entirely. The response to the delay proposal appears similarly inconclusive:

In a September 2025 statement in E&E News, the President of LNG Allies, the US trade group representing liquefied natural gas (LNG) industry interests, characterized the proposal as “shoot(ing) a hole in anyone who would be advocating for there to be equivalent before the Europeans,” effectively suggesting that the proposed suspension undermines US efforts to advocate for equivalence with EU methane reporting standards.

In the same article, an anonymous oil and gas lobbyist is quoted indicating that industry had hoped the EPA would not “go this far” and had advocated against the reconsideration.

API, which had previously urged the Administration to make revisions to the GHGRP, gave the New York Times the following statement on the proposal: “the oil and gas industry has a long track record of reporting greenhouse gas emissions to a variety of stakeholders, and we remain committed to doing so in a transparent and accurate way.”

Two other trade groups which had been consistently advocating to amend the methane reporting rules, the Independent Production Association of America (IPAA) and AXPC, do not appear to have issued any statements on the delay proposal.

US oil and gas industry associations appear to be hedging their bets: lobbying in favor of a weaker implementation of the methane import standard in the EU, while stopping short of publicly opposing the dismantling of domestic methane regulations such as the GHGRP to maintain chances of US equivalency. The EPA has published a docket for regulatory comments on the reconsideration of the GHGRP, with submissions due by November 3, 2025, presenting an opportunity for corporates to advocate for a strong GHGRP to preserve US energy’s global competitiveness and maintain regulatory stability in US methane policy. Once published, InfluenceMap will assess the responses to analyze how energy companies position themselves amid growing pressure to align with international methane reporting standards.