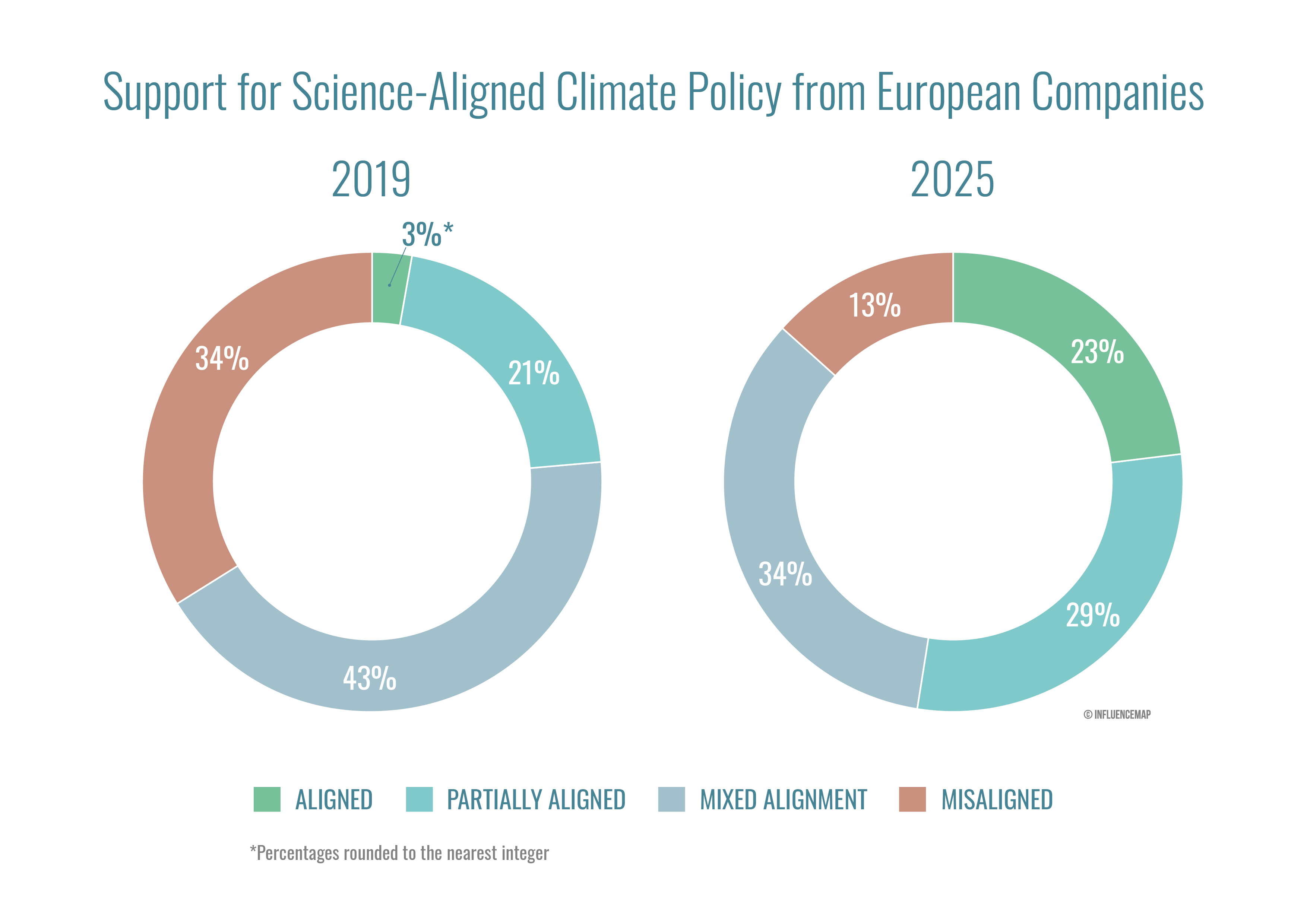

New analysis from the LobbyMap platform reveals a profound shift in corporate attitudes toward climate policy among businesses in the European Union1. 52% of European companies tracked by the platform now demonstrate science-aligned or partially science-aligned climate policy engagement, indicating broad support for the Green Deal’s agenda2. This marks a significant increase from 24% since the presentation of the EU Green Deal at the start of the 2019 legislative cycle. Meanwhile, the proportion of companies with misaligned climate policy engagement has dropped from 34% to 13% over the same period.

The findings challenge narratives promoted by certain industry associations since before the 2024 European Parliament elections which portray European industrial competitiveness as being in conflict with ambitious EU climate policy. These narratives appear to have exerted significant influence on the European Commission’s emerging climate policy agenda for 2024–2029.

The briefing highlights the impact of climate advocacy by industry associations representing sectors such as chemicals, construction, and automotives at the EU level, as well as cross-sector industry associations advocating for business interests in specific EU member states (e.g., Italy, Germany, and France). Over the past few years, these groups have resisted aspects of European climate policy ambition by deploying tactics like emphasizing the potential negative impact of climate policies on European “competitiveness,” advocating for incentive-based (“carrot”) approaches while opposing binding regulations, and promoting ambiguous policy terminology to leave the door open to continued reliance on fossil fuel technologies.

The briefing indicates that such arguments are likely inconsistent with the analysis provided by the Intergovernmental Panel on Climate Change (IPCC), as well as the diagnosis and solutions outlined in the 2024 Draghi report report on enhancing European industrial competitiveness. Moreover, they are at odds with the advocacy of a growing cohort of European corporate climate policy leaders in sectors such as power, industrials, and consumer staples. The findings raise ongoing concerns about the “lowest common denominator” effect, wherein industry associations are drawn towards the positions of a small proportion of their members (often from the fossil fuel value chain) that advocate most strongly and negatively on regulatory proposals to tackle climate change.

The use of detailed, positive advocacy on climate policy by an increasingly substantial portion of the corporate sector likely reflects the long-term nature of corporate investment cycles that are not easily swayed by shorter-term political developments. The results of this study aligns with recent polling of business leaders, which found that 97% of executives support transitioning from fossil fuels to a renewable-based electricity system. The businesses surveyed emphasized access to renewable electricity as a key factor in making long-term investment decisions and determining the competitiveness of regions to locate their operations and supply chains.

The ongoing debate over whether climate policy action strengthens or weakens international competitiveness is already influencing EU climate policy decision-making. For instance, the European Commission's Clean Industrial Deal prominently highlights issues such as reducing red tape and the need for technology-neutral energy policies. The EU’s ability to fulfill its international climate commitments in the coming years will likely depend on the impact of corporate policy advocacy on a range of key policies including the EU Carbon Border Adjustment Mechanism (CBAM) revision, sectoral decarbonization strategies, and future energy sector policies upcoming in the Affordable Energy Action Plan announced as part of the Clean Industrial Deal.

1 This study considers nearly 200 companies with legal domicile in "EU plus" (EU Members and the UK, Norway, Iceland, Switzerland, and Liechtenstein). It does not include US companies with significant European operations nor does it include "reverse headquarters" companies who have switched domicile to Ireland, for example from the US.

2 Science-Aligned Climate Policy Engagement is where an entity's positions on and efforts to influence climate-related government policy align with the global scientific consensus on what needs to happen to deliver the temperature goals of the Paris Agreement.

Recent polling shows that business leaders overwhelmingly support a rapid transition to renewable energy. Now, this research from InfluenceMap reveals that companies are acting on that strategic direction and treating climate action as material to their business. This is not the preoccupation of a minority, but an increasingly significant portion of the corporate sector that use science-aligned policy engagement as a tool for safeguarding strategic investments in the energy transition. It is incumbent on the rest of the business and investor community to take note of these positive trends. The case is clear: reducing emissions offers a pathway to operational efficiencies, greater resilience and reduced risk. Companies must take proactive steps to ensure their lobbying and association memberships support – not undermine – their business goals.

This briefing provides an overview of the LobbyMap platform’s analysis of corporate and industry association climate policy engagement in the European Union. The findings are split into two sections: first, overviewing the evolution of corporate climate policy engagement over the previous legislative term (2019–2024), and, second, examining how industry advocacy is influencing the development of the EU’s climate policy agenda for the next legislative term (2024–2029).

InfluenceMap’s LobbyMap platform tracks and assesses corporate climate policy engagement and covers over 1000 companies and 330 industry associations. This analysis draws from a sample of nearly 200 European companies and 80 industry associations (see InfluenceMap’s LobbyMap Platform for details). The companies covered are non-financial entities with legal domicile in "EU plus" (EU Members and the UK, Norway, Iceland, Switzerland, and Liechtenstein). It does not include US companies with significant European operations nor does it include "reverse headquarters" companies who have switched domicile to Ireland, for example from the US.

The LobbyMap methodology uses a definition of policy engagement based on the 2013 UN Guide for Responsible Corporate Engagement in Climate Policy. The focus of this analysis is company engagement with existing, evolving, and likely future policy measures issued by mandated bodies (e.g. the European Commission) to mitigate climate change by reducing greenhouse gas (GHG) emissions from the real economy. The analysis included in this briefing does not cover engagement with regulations focused on the financial system, including the development corporate reporting rules such as the Corporate Sustainability Reporting Directive (CSRD).

Evidence of corporate and industry association policy engagement is tracked in near real time across a range of publicly available data sources and scored against authoritative and external benchmarks to understand the level of support or opposition to policy that can deliver the 1.5ºC goal of the UN Paris Agreement. These benchmarks include government policy benchmarks, drawn from the original statements and ambitions of governmental bodies mandated to act on climate (e.g., the EU Commission), and science-based policy benchmarks, drawn from the guidance of the Intergovernmental Panel on Climate Change (IPCC) on the policy and technology pathways needed to deliver the Paris Agreement’s 1.5ºC temperature goal.

This section outlines the profound shift in corporate and industry attitudes toward science-aligned climate policy in the European Union since the start of the previous EU legislative cycle in 2019.

European headquartered companies have become significantly more supportive of science-aligned climate policy since the start of the 2019 European legislative cycle. Analysis from the LobbyMap platform’s assessment of nearly 200 European headquartered companies shows that the proportion of companies assessed to have fully aligned their climate policy advocacy with science-aligned policy has risen from 3% in 2019 to 23% in 2025. Conversely, the share of misaligned companies has dropped from 34% to 13%. This shift tracks the evolution of the European Green Deal, which was proposed and implemented between 2019–2024. The evolution in corporate attitudes in broad support for policies such as the Climate Law, the reforms of the Energy Performance of Buildings Directive, the Renewable Energy Directive, and the Energy Efficiency Directive appears to contradict the prevailing narrative that European business supports deregulation on climate.

The findings are significant as they contrast with recent political and economic developments in Europe and globally, which may appear to deprioritize the climate agenda for many companies. On the contrary, the results suggest that an increasingly substantial portion of the corporate sector — particularly those linked to the clean energy and technology value chains, (including highly significant demand-side sectors) — views climate policy as a long-term, business-critical issue.

These results align with recent polling of business leaders, which found that 97% of executives support transitioning from fossil fuels to a renewable-based electricity system. The businesses surveyed emphasized access to renewable electricity as a key factor in making long-term decisions, such as where to invest and where to locate operations and supply chains. The steady and growing use of detailed, positive advocacy on climate policy likely reflects the long-term nature of corporate investment cycles, which now need to be secured and protected, and that are not easily swayed by short-term political developments.

The LobbyMap platform also assesses 80 industry associations that are actively engaging with climate-related policy at the European level. Analysis of these groups shows steady improvements in their positioning on climate-related policy over time, with aligned entities increasing from 2% to 12% between 2019 and 2025. However, the rate of change does not appear to match the more profound shift in attitude amongst the European companies assessed.

This briefing focuses on 25 highly significant industry associations at the EU level—including the 20 most engaged industry associations on climate-related policy in Europe (including groups representing key industries from a climate perspective such as automotive, aviation, steel, chemicals, and power) as well as several important country-specific and EU-level cross-sector industry associations.

Industry associations representing heavy industry (e.g., steel, cement, chemicals) and transport (e.g., automotive and aviation) have seen improvements in their LobbyMap scores since 2019 but retain a significant level of resistance to ambitious climate policy in the region. Key policies of concern include the EU Emissions Trading System (EU ETS) Reform, the Carbon Border Adjustment Mechanism (CBAM), and the Heavy Duty Vehicle CO2 Targets.

Prominent cross-sector industry associations at the EU level (BusinessEurope) and representing member states, including France (Mouvement des Entreprises de France (MEDEF)), Spain (Spanish Confederation of Business Organizations (CEOE)), Italy (Confederation of Italian Industry (Confindustria)), and Germany (Federation of German Industries (BDI)), are some of the most negative voices on climate policy in the region. This is despite these groups nominally representing a broad base of sectors and businesses that InfluenceMap’s analysis suggest take more supportive stances. These findings raise ongoing concerns around the 'lowest common denominator' effect, in which industry associations represent the positions of only a small proportion of their members that advocate most strongly and negatively on regulatory proposals around climate.

By contrast, another set of industry associations has been pushing for increased speed and ambition on policy that can support a swift energy transition in Europe.

Industry groups pushing a renewable agenda (e.g. WindEurope and SolarPower Europe) have been highly active, including campaigning for ambitious revisions of the Energy Performance of Buildings Directive, the Renewable Energy Directive, and the Energy Taxation Directive. These are joined by Eurelectric, which has actively promoted the role of electrification as a key decarbonization pathway for sectors such as transport, housing, and industry.

In addition, seemingly filling the gap left by traditional cross-sector industry associations that remain oppositional to climate policy ambition, alternative groups have emerged to represent a range of pro-climate companies on EU climate policy. The Corporate Leaders Group (CLG), which counts among its members companies from utilities, industrials, consumer goods, and information technology sectors, is an example. Between 2019–2024, CLG campaigned successfully on policy issues including the Renewable Energy Directive and Energy Performance of Buildings Directive reforms.

Finally, the European Round Table for Industry (ERT), a highly significant cross-sector group that represents the leaders of the largest companies in Europe, has also shifted its positioning towards greater support for climate policy in recent years. Despite retaining unsupportive positions on policies such as EU ETS reform and the CBAM, the ERT has become a prominent and positive advocate on policy issues such as the Energy Efficiency Directive and the Renewable Energy Directive delegated acts on renewable hydrogen and recycled carbon fuels. InfluenceMap now assesses the ERT to be notably more positive on climate policy than many of its EU-focused cross-sector industry association peers.

This section tracks how a subgroup of European industry has pushed a set of narratives and arguments emphasizing concerns around the impacts of European climate policy on international competitiveness in the run up to and following the 2024 European Parliament elections. Despite a separate group of European industry associations challenging these narratives, they appear to have had a significant impact on the policy agenda for the 2024–2029 European legislative cycle.

Due to geopolitical events occurring between 2022 and 2024 that affected Europe’s regional and diplomatic partners, maintaining balance between climate objectives and economic prosperity has become a key theme for European policymakers. In 2021, the European Commission introduced the ambitious Fit for 55 Package, a set of proposals including targets, standards, incentives, and regulations to meet its goal of reducing net greenhouse gas emissions by at least 55% by 2030 and achieve climate neutrality by 2050. However, Russia’s invasion of Ukraine in February 2022, which intensified an energy price crisis that had already begun in late 2021, shifted the Commission’s focus toward addressing Europe’s reliance on energy imports, particularly from Russia.

Meanwhile, the US introduced the Inflation Reduction Act (IRA) in August 2022, which directed significant funding and support to domestic ‘clean’ technology development. In an attempt to respond to these developments, the EU Commission introduced the Green Deal Industrial Plan in February 2023. Unlike the Fit for 55 Package, which focused on regulatory measures to decarbonize traditional industries, the Green Deal Industrial Plan and its Net-Zero Industry Act aimed to provide financial support and incentives for scaling up new low-emission technologies and industries. This marked a shift toward placing industrial policy and competitiveness at the center of EU climate policy.

In the run up to the 2024 European elections, rising concerns over the cost of living became the backdrop to a growing backlash against EU green policies, prominently driven by right-wing political parties. Concurrently, powerful actors within EU industry ramped up their promotion of narratives that centered international competitiveness as a key issue for the 2024–29 policy agenda. Concern over European climate policy ambition subsequently re-emerged as a mainstream political concern.

A review of European industry associations’ pre-election policy papers (published between July 2023 and May 2024, setting out each industry association’s priorities for the forthcoming legislative cycle) indicates a significant effort to shape the narrative around future European climate policy in the run up to the European Parliament’s 2024 elections. Analysis of over 20 pre-election policy papers from industry associations previously found to be resistant to EU climate policy ambition identified three common arguments or tactics:

In its manifesto for the 2024–2029 EU legislative term (published July 2023), the European Chemical Industry Council (Cefic) indicated that “overly detailed legislative proposals” are impacting corporate international competitiveness, alongside the energy crisis. It suggested that such a legislative environment is slowing the transition to climate neutrality while creating an unfavorable investment climate in Europe.

European Steel Association (Eurofer)’s February 2024 manifesto called into question the impact of legislating an ambitious EU 2040 climate target and instead argued that climate ambition should instead be delivered through “innovation and investments.”

In its February 2024 manifesto, the Italian Confederation of Industry (Confindustria) advocated for a technology neutral approach to the EU’s policies to decarbonize mobility.

The February 2024 Antwerp Declaration was coordinated by the European Chemical Industry Council and “73 business leaders spanning 17 sectors.” The Declaration constituted a statement to the European Commission President, Ursula von der Leyen, and Belgian Prime Minister, Alexander De Croo, calling for “a European Industrial Deal to complement the EU Green Deal.” Despite indicating support for the EU Green Deal and the EU’s climate targets, the declaration urges EU policymakers to avoid implementing prescriptive regulations to follow EU climate targets and stresses the need for revisions to EU policies to protect EU industry’s international competitiveness. More specially, the Declaration appears to advocate for a form of policymaking that relies on incentives and a limited regulatory framework. Some of the 10 recommendations make references to an energy transition that reflect guidance from the Intergovernmental Panel on Climate Change, such as the need for grid expansion, electrical power, and hydrogen. However, it is not clear that these recommendations are explicitly IPCC aligned due to the vagueness of the language used. The EU Commission appears to have engaged closely with the corporate sector to develop the Clean Industrial Deal based on industry’s demands. The Commission’s 2025 proposal for a Clean Industrial Deal explicitly confirms that the measures proposed are the direct result of stakeholder engagement through processes such as the Antwerp Declaration and the Clean Transition Dialogues initiated by Ursula von der Leyen in her 2023 State of the Union speech.

EU industry employed the arguments detected in the industry associations’ policy priority documents for the 2024–29 European policy cycle and elements of the Antwerp Declaration to hold back or weaken specific climate policies in 2022–24. These narratives have been deployed in a manner that does not appear consistent with the IPCC’s guidance on 1.5°C-aligned policy pathways.

For example:

| Narratives | Industry Use of Narrative (2019–2024) | Analysis of Narrative Against IPCC Guidance on 1.5°C-aligned Policy Pathways |

|---|---|---|

| Climate policy risks competitiveness | Certain European industry associations—including Confindustria, MEDEF, and Airlines for Europe—frequently emphasized the need to protect international competitiveness when pushing for weaker EU carbon pricing policies, such as the Carbon Border Adjustment Mechanism (CBAM) and the reform of the Emissions Trading System (ETS), as well as policies tackling emissions from transportation, energy, and the food system. | While there is no intrinsic reason why promoting competitiveness should equate to opposition to climate policy, European industry players have leveraged related concerns to push a deregulatory agenda on climate. This messaging is inconsistent with the findings outlined in the IPCC’s 2022 Mitigation of Climate Change Report (AR6) that found that, as of 2022, there is no consistent evidence that climate policy negatively impacts companies’ international competitiveness through carbon leakage. |

| Supporting policy carrots, while opposing regulatory sticks | Several associations—including the BDI, Eurofer, and BusinessEurope—pushed for EU climate policies to focus on incentivizing investment over and/or instead of regulatory measures, including in the Net-Zero Industry Act, the Industrial Carbon Management Strategy, the Electricity Market Design Reform, and even the European Green Deal as a whole. | While support for incentives for climate technologies is aligned with IPCC guidance, combining these demands with a push to weaken or roll back regulatory measure is not. The IPCC’s 2018 Special Report on Global Warming of 1.5°C (SR15) found that low-carbon investments are facilitated by a coherent policy framework including both stringent standards and technology policies. Explicit carbon pricing, direct regulation, and public investment to enable innovation are critical for deep decarbonization pathways . |

| Promoting vague policy terminology | Associations—including Eurofer, Confindustria, FuelsEurope and CEOE—promoted integrating vague terms and approaches, such as ‘technology neutrality,’ in policies, while advocating to weaken climate policy ambition. For example, associations used this narrative when engaging on the Electricity Market Design Reform, theCO₂ Emissions Standards for Heavy-Duty Vehicles and Light Duty Vehicles, and the Net-Zero Industry Act. | The principle of ‘technology neutrality’ can be broadly science-aligned if communicated with clear guardrails on the need for technologies to deliver specific emissions reductions. However, the term has instead been used by industry advocates to promote future roles for fuels and technologies that do not align with IPCC guidelines. The IPCC’s 2018 Special Report on Global Warming of 1.5°C (SR15) also found that greater success comes when government policy prioritizes selected technologies and pathways to decarbonize specific industries, such as electrification and renewable energy. |

The much-anticipated 2024 Draghi report on European competitiveness also appears to challenge the way in which industry actors have deployed certain narratives to oppose European climate policy ambition. Instead, it highlights alternative reasons for a lack of European industrial competitiveness and prescribes significant policy reform while maintaining core climate regulations to enable a ramp up in climate action.

The theme of ‘sustainable competitiveness’ is central to the much anticipated 2024 report from former European Central Bank President Mario Draghi, which outlines recommendations to spur economic growth in the EU. In contrast to narratives that industry actors pushed in 2024–25 that suggest that European climate policies are endangering European international competitiveness, the Draghi report points to high and volatile energy prices (stemming from a reliance on fossil fuels), lengthy permitting procedures, and energy taxation that currently favors fossil fuel consumption. The report recommends an increase in investment in the decarbonization of the economy, simplifying and streamlining permitting and administration processes for renewables, and improving grid and flexibility infrastructure through reforms to the EU’s energy market. To help tackle competitiveness issues, the report advises on the need for increased investment in ‘clean’ technologies and proposes concentrating on scaling up European manufacturing by providing it with enough cheap gas in the short term alongside a longer-term focus on decarbonized electricity. The report supports the implementation of the EU ETS and CBAM, and it does not advise that governments scale back the ambition of EU climate regulations. While the report does appear to promote adopting a ‘technology neutral’ approach to accelerating decarbonization, it references specific technologies that should be promoted under such an approach. It does not leverage this argument to challenge the objectives of sector specific policy instruments already agreed upon and adopted by the EU.

Growing evidence from the LobbyMap database indicates that business groups promoting science-aligned climate policy are challenging narratives that pit competitiveness against climate action. This evidence indicates the development of a counter narrative arguing that robust and clear climate policy and regulation can in fact enhance European competitiveness on an international scale:

Corporate Leaders Group (CLG) advocated for the EU to bolster competitiveness by increasing the ambition of government regulation on climate change and opposing any deregulation or backtracking on long-term policies in the name of maintaining a consistent regulatory landscape to encourage growth. Corporate Leaders Group (CLG) also supported a science-aligned 2040 Climate Target of 90% to improve the EU’s competitiveness and resilience to shocks.

Associations representing the renewable energy industry advocate that energy sources such as wind and solar are key for preserving the EU’s international competitiveness. SolarPower Europe highlights a range of climate regulations that are key to bolster renewable energy development in the EU and consequently improve industrial competitiveness, such as the Net-Zero Industry Act, the Electricity Market Design Reform, the Renewable Energy Directive, and the Energy Taxation Directive.

On certain climate policy issues, heavy industry groups that have elsewhere expressed caution on climate policy ambition have joined renewable energy and electric power associations to emphasize the economic benefits of the energy transition.

In joint recommendations from the Antwerp Dialogue on Industrial Electrification and Competitiveness, industry associations—including Eurelectric, WindEurope, SolarPower Europe, Cefic, Eurofer, Cembureau, Eurometaux, and the Confederation of European Paper Industries—recognized that scaling up direct and indirect industrial electrification, improving grid infrastructure, and boosting the scale up of decarbonization technologies are crucial to support the EU’s industrial competitiveness and achieve a climate neutral economy by 2050.

The publication of the EU Commission’s January 2025 Competitiveness Compass and February 2025 Clean Industrial Deal indicates that the industry narratives identified in this briefing are playing a significant role in shaping the climate policy agenda for the next EU legislative cycle. Industry debate over how to address preserving international competitiveness and EU climate action appears to have had a particular influence on the strategy.

The European Commission’s January 2025 Competitiveness Compass proposed to “regain competitiveness and secure sustainable prosperity,” and the Clean Industrial Deal released in February 2025 aimed to accelerate industrial decarbonization while boosting the EU’s traditional heavy industries and emerging clean technology sectors. The documents re-affirm the Commission’s commitment to the EU’s 2050 climate neutrality target and maintain the proposed 2040 GHG emissions reduction target of 90%. They also announce an economy-wide electrification target of 32% by 2030, as well as a target of 100 GW of renewable electricity installation in the years up to 2030, which are consistent with demands from CLG, for example.

However, while the Commission has stated that it will maintain alignment with the European Green Deal, certain proposals appear to align with advocacy from industry associations on the need to ‘cut red tape’ across a range of policies including the CBAM, as well as the need for a ‘technology-neutral’ approach to policies such as the Action Plan for Affordable Energy. In the lead up to and in response to these announcements, industry associations such as BusinessEurope have continued to push for deregulation and technology-neutral policy approaches. InfluenceMap’s analysis shows how such industry advocacy has already begun impacting the development of specific EU climate-related regulations for industry:

In December 2024, industry associations including BusinessEurope and Copa-Cogeca successfully advocated for a 12 month delay to the implementation of the EU Regulation on Deforestation-free Products (EUDR) and asked the Commission to explore further simplifications of requirements.

Industry demands, voiced by MEDEF, Confindustria, and BusinessEurope, were reflected in the EU Commission’s proposal to scale back CBAM requirements in the Clean Industrial Deal in February 2025.

Several associations—including BusinessEurope and Eurofer—are now calling for additional policies, such as the EU ETS, the Critical Raw Materials Act, the Packaging and Packaging Waste Regulation, and the Net-Zero Industry Act, to be ‘simplified.’ Policies that have yet to be finalized, such as the Hydrogen and Gas Package Delegated Act on the definition of low-carbon hydrogen, now face similar industry-driven pressure. For example, groups including Cefic and Eurofer are pushing for a technology neutral approach to EU hydrogen policies rather than the EU’s current legislative approach which prioritizes scaling up renewable hydrogen.