Many fund managers have abandoned their climate-related fund names since the commencement of European Securities and Markets Authority (ESMA) fund naming guidelines in May 2025. Use of “ESG” and “Sustainability,” specifically, dropped by over 25% after the rules took effect, reflecting concerns about potential greenwashing in the sector over the past years. Below, we update our earlier assessment of EU-based funds with new analysis on the impact of the guidelines.

In December 2024, FinanceMap released a climate assessment of EU-based funds in light of the proposed ESMA fund naming guidelines and the existing Sustainable Finance Disclosure Regulation (SFDR). We found that, as of June 2024, EU-based “ESG” equity funds were more invested in fossil fuel1 companies than green2 companies, while funds using “Environment,” “Transition,” and “Impact” naming invested on average at least four times more in green companies than fossil fuel companies.

The EU fund market has since reacted to the May 2025 implementation of the ESMA guidelines. FinanceMap’s latest analysis of EU-based funds reveals that, between June 2024 and May 2025, the number of funds with “ESG” and “Sustainable” in their names decreased by 28% and 27%, respectively. Over the same period, “ESG” and “Sustainable” equity funds simultaneously decreased their fossil fuel investments and increased their green exposure. The number of funds using “Transition”-related names, meanwhile, grew by 10%, and these increased their exposure to both fossil fuel and green companies.

The new ESMA criteria for funds using climate-related names include:

The table below shows the change in the number of funds using ESG or climate-related terminology from June 2024 to May 2025.

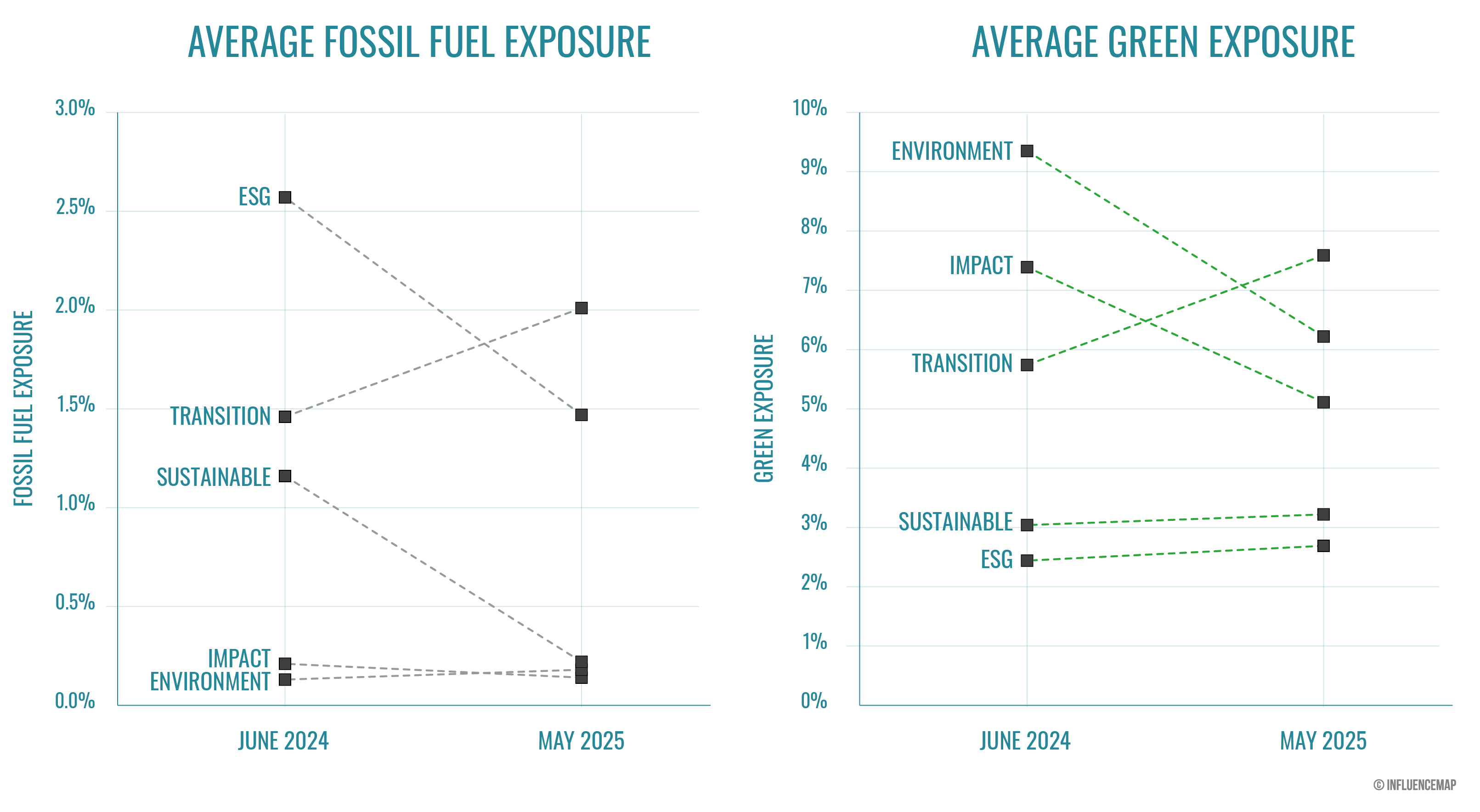

FinanceMap’s analysis finds that the average “Transition” fund increased its exposure to fossil fuel companies from 1.5% in June 2024 to 2.0% in May 2025. In contrast, the average fossil fuel exposure of “ESG” funds fell from 2.6% to 1.5%, and “Sustainable” funds reduced their exposure from 1.2% to 0.2%. Meanwhile, “Environment” and “Impact” funds decreased their exposure to companies identified as green, while “Transition,” “ESG,” and “Sustainable” funds increased their green exposure.

These findings indicate that the introduction of ESMA’s fund naming guidelines has had a significant impact on the ESG and climate-related fund market in the EU. The decrease in “ESG” and “Sustainable” fund names suggests that many fund managers, fearing non-compliance with ESMA guidelines, elected to remove the terms from fund names rather than meet the new criteria—indicating potential previous greenwashing. The removal of these appears to have left funds in these categories with lower fossil fuel exposure while retaining similar levels of green investment.

The growing popularity of transition-related funds, coupled with their increased fossil fuel exposure, shows that greenwashing risk may persist in EU markets in the form of transition investing.

1 Fossil fuel companies are defined as companies primarily active in fossil fuel production value chains.

2 Green companies are defined as companies deriving at least 75% of revenue from EU taxonomy-aligned activities.

3 This includes “ESG.” While ESMA includes “ESG” terms in the “Environment” category, this research chooses to disaggregate the two to demonstrate the substantial difference in the climate performance of funds using these terms.