This online briefing is the second in a recently launched regular series providing an overview of corporate policy engagement on methane policy globally as captured on InfluenceMap’s Methane Platform. The briefing analyzes recent corporate engagement on methane policies and explores the narratives adopted by industry to restrict action on methane emissions.

The briefing highlights the initial industry resistance to Denmark’s pioneering emissions tax targeting agricultural methane emissions, outlines how the outcome of the US election could significantly impact the country’s methane regulatory efforts, and discusses how the EU’s Methane Regulation can provide a strong benchmark for methane reduction policies in Asia.

Denmark's announcement of an emissions tax on agricultural methane makes it the first country to legislate methane reduction in the sector, setting a crucial baseline for global methane reduction efforts. Following the announcement, the Danish food and agriculture industry has pushed back against the policy. While a similar effort in New Zealand was halted after a change in government, Denmark now has the opportunity to set a strong benchmark for ambitious methane reduction in agriculture.

The Biden administration has taken significant steps to address methane emissions, implementing updated regulations, revised reporting requirements, and a methane emissions charge. However, the oil and gas industry has actively lobbied to oppose and weaken these efforts. The upcoming 2024 US election could disrupt this progress, as Republican candidate Donald Trump, supported by oil and gas industry interests, may seek to rollback regulatory advances.

The EU Methane Regulation’s inclusion of imported fossil fuels sets a precedent for Asian fossil fuel importers to address methane emissions across their supply chains. Countries like China, Japan, and South Korea have already shown interest in controlling methane emissions through emission reduction plans and joint declarations. The EU regulation establishes a benchmark for future methane policies and regulations that will be vital for achieving global methane reduction targets.

The fossil fuel industry, led by Eurogas and the International Association of Oil and Gas Producers (IOGP), has pushed the narrative that methane regulations harm energy security in its advocacy on the EU Methane Regulation. Analysis reveals that these associations consistently promoted this claim throughout the policymaking process (2022–24), despite evidence from the Intergovernmental Panel on Climate Change (IPCC) and International Energy Agency (IEA) showing that methane regulations actually bolster energy security. This narrative could potentially emerge in other regions as they consider adopting similar methane policies.

Despite new policies and voluntary measures announced in the past year to address methane emissions, global methane levels are reported to be “rising rapidly” and are expected to continue increasing through the decade without immediate, drastic action. Since pre-industrial times, methane has accounted for 0.5 °C of global warming, compared to 0.8 °C from carbon dioxide. Key developments that will significantly impact the success of efforts to reduce methane emissions are highlighted below:

Denmark picks up where New Zealand left off on Agricultural Methane: In June 2024, Denmark announced its Agricultural Emissions Tax, aimed at addressing methane emissions and other pollutants from the livestock industry. This marks the first policy globally to legislate agricultural methane emissions. The tax is part of a wider policy package on agriculture and food production that is estimated to reduce Denmark’s emissions by 1.8 million metric tons of CO₂-e in 2030, helping the country meet its 2030 and 2050 climate targets. New Zealand previously proposed a similar initiative, the farm-level split-gas levy, in October 2022, which sought to tax agricultural methane emissions instead of including them in the country’s emissions trading scheme. However, following the change of government after the October 2023 general election, the policy stalled with minimal progress, giving Denmark an opportunity to set a high benchmark for ambitious action on agricultural methane emissions. Initial parliamentary discussions began early September, and further negotiations are expected later this year.

US Election Puts Methane Policy Progress at Risk: The Biden administration has made significant strides in addressing methane emissions from the oil and gas sector, introducing updated methane emissions standards (EPA Methane Regulations), revised reporting requirements (EPA Methane Reporting Revisions), and the Methane Fee (Methane Emissions Charge (IRA)). The policies aim to improve the detection and repair of methane emission leaks from new and existing wells, establish a comprehensive emissions reporting framework, and impose penalties for non-compliance. However, the upcoming US presidential election in November 2024 poses a potential challenge to this progress. Republican candidate Donald Trump has strong backing from the oil and gas industry, which has reportedly pressured Trump to rollback methane regulatory advancements. InfluenceMap’s data finds significant oil and gas industry pushback on methane regulations since the beginning of the Biden administration.

Opportunity for Fossil Fuel Importers in Asia to Tackle Methane: The European Union’s inclusion of imported fossil fuels in its newly adopted Methane Regulation serves as a crucial benchmark for other major fossil fuel importers to consider for new methane policy. Key countries in Asia, including China, Japan, South Korea, and India, are all major fossil fuel importers and therefore will play a key role in reducing global methane emissions. While there has been limited progress in Japan and India on methane policy, China and South Korea have released methane emission reduction plans. Additionally, in July 2023, Japan and South Korea signed a joint statement on ‘Accelerating methane mitigation from the LNG value chain,’ highlighting the potential for meaningful policy on methane emissions in the region.

The analysis for corporate engagement on specific methane policies is derived from InfluenceMap's Methane Platform. To explore the underlying evidence further, click on the hyperlinks throughout the section.

Denmark’s coalition government announced its proposed tax on agricultural emissions in June 2024, following months of fraught negotiations with leading industry, agricultural, and environmental groups. If passed, farmers will pay 120 Danish kroner (DKK) per metric ton of CO₂-equivalent emissions starting in 2030, increasing to 300 DKK in 2035. The levy primarily targets methane emissions from ruminant livestock, as well as other gases from fertilizers, forestry, and the cultivation of carbon-rich soils.

The tax is one component of the Agreement on a Green Denmark, a comprehensive policy package aimed at restructuring Danish agricultural and food production, alongside other land reform measures including wetland restoration and afforestation. The agreement is estimated to reduce Denmark’s emissions by 1.8 million metric tons of CO₂-e in 2030, ensuring that the agriculture sector contributes to the country’s 2030 and 2050 climate targets.

The committee tasked with settling the agreement, the Green Tripartite, includes ministers, figures from municipal governments and environmental organizations, and representatives from industry groups such as Landbrug & Fødevarer (Danish Agriculture & Food Council), Fødevareforbundet NNF (Food Union NNF), Dansk Metal (Danish Union of Metalworkers), and Dansk Industri (Confederation of Danish Industry).

Proposals to the Tripartite by a green tax reform expert group in February 2023 included three different tax models ranging from 125 to 750 DKK. To varying degrees, these models balance the tax’s financial burden on wider Danish society, effectiveness at reducing emissions, and risks to industry jobs and production.

The true cost of the tax is higher than the effective rates imply, starting at 300 DKK per metric ton in 2030 and rising to 750 DKK in 2035. This is because the Tripartite negotiated a floor tax deduction of 60% while the measure is phased in to limit the impact on production costs and provide an economic advantage to already climate-efficient farmers. Proceeds from 2030–2031 are set to be pooled and returned to the industry as a green transition support fund.

Engagement with the agricultural emissions tax from the corporate sector thus far is generally unsupportive:

Following the release of the three considered tax models, CEO messaging from regional food companies Danish Crown and Arla Foods appeared to oppose all proposed levels of ambition for the policy. The companies expressed reservations that any tax on agricultural emissions would bring about production declines and emphasized green innovation as their preferred route for the sector's transition.

In response to the finalized proposal’s announcement, Arla’s CEO leveled criticism that a tax would “economically penalize” farmers already engaging in the green transition, although later comments to POLITICO hailed the legislation as a “well-balanced and clever piece of work.”

Campaign group European Livestock Voice deflected from the agricultural industry’s methane emissions by emphasizing emissions from landfills and the oil and gas industry in its coverage of the policy.

The Danish Parliament began debating the agricultural emissions tax in early September, and negotiations are expected to continue later this year. It remains to be seen how this corporate engagement will shape the policy throughout the upcoming political process, with some concessions to industry appearing in the original proposal.

In January 2024, the US Environmental Protection Agency (EPA) proposed official guidance for implementing the Inflation Reduction Act’s methane fee (the waste emissions charge), following an earlier request for information in December 2022. The latest regulatory agenda suggests that this guidance may be finalized by the end of the year.

The proposed guidance sets parameters for meeting the methane fee, which applies to oil and gas facilities that report more than 25,000 metric tons of CO₂-e per year, beginning at $900 per metric ton of methane reported in 2024 and increasing incrementally to $1,500 by 2026. The fee is calculated using the revised methane reporting assessment criteria, which were finalized in May 2024, and complemented by the EPA’s methane regulation — which was finalized in December 2023—in that companies that do not comply with the regulation will be subject to the fee.

In its implementation guidance, the EPA proposed three possible exemptions from the methane fee that are available to companies that exceed the waste emissions threshold:

“Unreasonable delay” in environmental permitting, which is defined by a set of four criteria that must all be met in order to qualify for the exemption;

Regulatory compliance for facilities that meet the methane regulation once all federal and state implementation plans have been approved, among other qualifications; and

Plugged wells, only in the onshore and offshore petroleum and natural gas production industry segments, that have been “permanently shut-in or plugged” in the previous year in compliance with closure requirements.

InfluenceMap has identified concentrated efforts from the oil and gas industry to weaken the implementation of the methane fee, outlined below:

Strong Industry Opposition to EPA’s Methane Fee: In March 2024, several industry groups, including the American Exploration and Production Council, American Fuel and Petrochemical Manufacturers, Western States Petroleum Association, Independent Petroleum Association of America (IPAA), and LNG Allies, signed the American Petroleum Institute’s (API) joint comments against the EPA's proposed methane fee. The letter called for less stringent requirements for exemptions and questioned the EPA’s legal authority to enact the fee. The IPAA also submitted its own comments criticizing the Waste Emissions Charge, labeling it as burdensome and economically detrimental. ConocoPhillips opposed the fee, advocating for less stringent emissions calculations and compliance exemptions, while also stating support for API's comments.

Advocacy for Flexible Netting Measures: Several major companies, including BP, Kinder Morgan, and Occidental Petroleum, have advocated for the EPA to allow netting of emissions at the parent company level. This would allow companies to offset high-emitting facilities with lower-emitting ones across their portfolios, potentially avoiding the methane fee if their net emissions are zero or negative. Large companies with many facilities could use this flexibility to avoid substantial reductions in overall emissions. By offsetting pollution at high-emitting sites with a few cleaner sites, this could effectively reduce or eliminate their fee liability without meaningfully cutting emissions. This would undermine the methane fee’s goal of reducing methane, which is over 80 times more potent than CO₂, over 20 years.

Calls for Weaker Implementation and Exemptions: Several companies and associations have advocated for a weaker implementation of the methane fee by requesting more exemptions. Coterra Energy emphasized numerous concerns around the fee, advocating for less stringent emissions calculations and additional exemptions for gas facilities. The American Gas Association (AGA) was similarly unsupportive of the fee, calling for exclusions of certain fossil gas facilities and more exemptions. American Exploration and Production Council (AXPC) called for greater flexibility and the exclusion of specific emissions to ease regulatory compliance.

Concerns About EPA’s Authority and Regulatory Approach: Industry lobbying efforts have also consistently stressed legal concerns around the EPA’s authority to implement the fee. The US Chamber opposed the methane fee, challenging the use of social cost of greenhouse gases (SC-GHG) values and alleging that the EPA exceeded its legal authority. IPAA also critiqued the regulation as economically harmful and burdensome, endorsing API's critical stance on the EPA’s regulatory reach.

Final guidance on the fee is expected later in 2024, with industry pushback likely to impact the rule’s ultimate ambition.

In December 2023, Canada announced updated draft regulations for the 2018 Regulations Respecting Reduction in the Release of Methane and Certain Volatile Organic Compounds (Upstream Oil and Gas Sector). With this update, the government aims to strengthen regulations to achieve its target of at least a 75% reduction of oil and gas methane emissions below 2012 levels by 2030. The new proposal would set a new standard for leak detection and repair (LDAR), including quarterly-based inspections at facilities. It also proposed a ban on venting, including from equipment such as pneumatic devices, and a new requirement to reduce the flaring of associated gas. The regulation would enable operators to adopt performance standards as an alternative to venting and flaring requirements. The regulation is set to be phased in beginning in 2027, with full uptake by 2030. InfluenceMap has detected highly negative engagement from the oil and gas sector to weaken the scope and key aspects of the regulations.

Advocacy to Weaken the Scope of the Regulations: Oil and gas entities such as the Canadian Association of Petroleum Producers (CAPP), Pathways Alliance, and Tourmaline advocated that the government’s 75% methane reduction target should exclude upstream mining emissions. Vermilion raised similar concerns and endorsed CAPP’s comments.

Criticizing the Leak Detection Criteria and Venting and Flaring Restrictions: Canadian Natural, ConocoPhillips, and MEG Energy appeared unsupportive of the restrictions on flaring and venting and criticized the frequency of fugitive emissions survey requirements. Shell supported the flaring provisions but advocated to weaken the criteria for venting. TC Energy opposed the monthly emissions screening requirements, while Enbridge raised concerns with the limitations on venting.

Advocating Against the Federal Government’s Regulatory Framework: Several oil and gas entities criticized federal regulation of methane, with many advocating for provincial jurisdiction over methane regulations. This includes CAPP, Cenovus, Enbridge, Pembina Pipeline, and Vermilion. A few entities, including Cenovus, Pathways Alliance, and MEG Energy, also emphasized the regulatory burden and opposed what they labeled as “prescriptive” measures in the regulation.

Following the December 2023 announcement, a public consultation was open until February 2024. The policy is likely to be finalized later this year, and significant industry advocacy to weaken the policy could result in a reduction in the strength of the regulations.

The Canadian government also announced draft regulations in June 2024 to tackle methane reduction in the waste sector. These seek to reduce methane emissions from landfills receiving municipal solid waste through a performance-based approach to identify methane leaks and ensure optimal methane recovery. The government announced that the 60-day public consultation is complete and stated that it is currently reviewing the comments. InfluenceMap will assess industry engagement once the consultation responses are released.

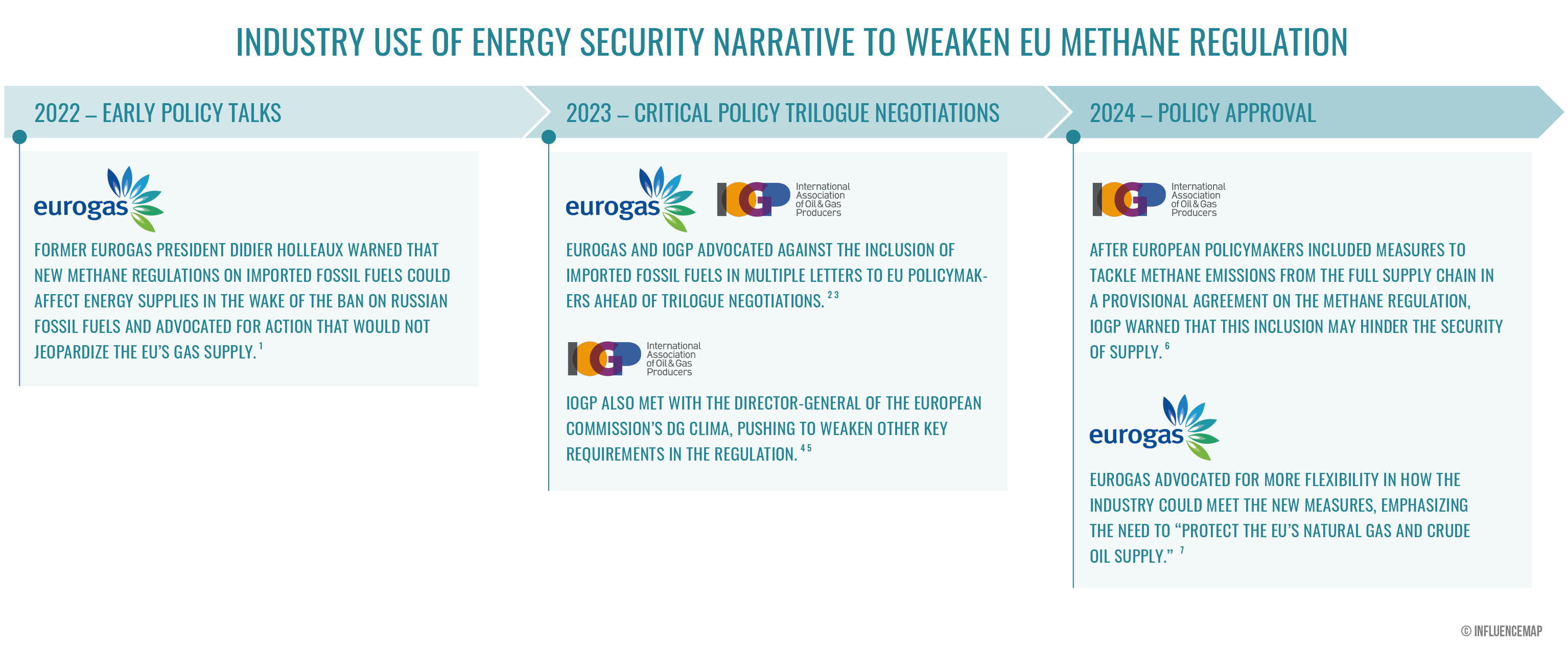

The previous Methane Bulletin highlighted how the oil and gas and agricultural industries adopted a playbook of narratives to restrict methane regulation. This edition delves into how several European oil and gas industry associations, including Eurogas and the International Association of Oil and Gas Producers (IOGP), have pushed the narrative that methane regulations harm energy security, particularly in response to the EU’s efforts to include imported fossil fuels in the scope of its policy.

Given the EU’s reliance on imports for over 80% of its fossil gas consumption, European policymakers have debated expanding the regulation to cover the full energy supply chain to act on imported fossil fuels. This move aligns with the EU’s commitment to reduce methane emissions from its fossil fuel supply chains, as it demonstrated when it signed the joint statement on ‘Accelerating methane mitigation from the LNG value chain’ in July 2023 alongside Australia, the US, Japan, and South Korea.

However, members of the European oil and gas sector pushed back on the EU’s attempt to consider the entire fossil fuel supply chain in the scope of its methane regulation. Notably, Eurogas and the International Association of Oil and Gas Producers (IOGP) accounted for nearly half of the identified claims that methane regulations would negatively impact energy security and production, and have undertaken this advocacy across key policy moments.

Authoritative bodies such as the Intergovernmental Panel on Climate Change (IPCC) and the International Energy Agency (IEA) have been clear in highlighting the climate, economic, and health benefits of reducing methane emissions. Regarding energy security, the IEA reported in 2022 that methane emissions regulations in the oil and gas sector could make an additional 210 billion cubic meters (bcm) of fossil gas available to global gas markets from gas resources currently lost to flaring and leaks in the supply chain. This could provide more immediate relief to energy security and supply concerns than investments in new gas supply.

The European Union’s inclusion of imported fossil fuels in its newly adopted Methane Regulation for the energy sector sets a benchmark for other major fossil fuel importers to address methane emissions from their supply chains. China and South Korea’s methane emissions reduction plans, along with Japan’s and South Korea’s signatures to the July 2023 joint statement on ‘Accelerating methane mitigation from the LNG value chain,’ highlight the potential for increased policy action on methane emissions in the region.

The industry’s use of narratives on energy security not only appears to be misaligned with findings from authoritative bodies such as the IPCC and IEA, but also poses a significant risk to the development of ambitious methane policy globally. This is especially relevant as other countries consider following the EU’s lead in addressing methane emissions across the entire supply chain.

1 February 2022 Euractiv article

2 August 2023 Joint Letter to EU Policymakers

3 September 2023 Joint Letter to EU Policymakers

5 Documents from October 2023 Meeting with DG CLIMA accessed via FOI

6 April 2024 Social Media post

7 May 2024 Press Release