This briefing provides an overview of the direct and indirect (via industry associations) engagement of Climate Action 100+ (CA100+) companies within the aviation and oil and gas sectors on SAF. It explores the narratives deployed by both industries to weaken or obstruct robust SAF policies, exploring engagement on the EU SAF mandate (ReFuelEU), the UK SAF mandate, and the US Clean Fuel Production Credit.

SAF refers to jet fuel alternatives that reduce lifecycle greenhouse gas emissions compared to conventional jet fuel. It can be produced from biological (bio-SAF) or synthetic (e-SAF) sources. Despite e-SAF offering greater potential for emissions reductions than bio-SAF, its production remains on a small scale. Bio-SAFs are associated with significant indirect greenhouse gas (GHG) emissions and have direct implications for carbon sinks, food security, and biodiversity.

InfluenceMap’s analysis reveals frequent advocacy by the aviation and oil and gas sectors to weaken mandates and sustainability safeguards. Many actors have pushed to amend feedstock eligibility under mandates. Key positions include pushing for the inclusion of crop-based feedstocks and advocating for a delay in implementation timelines.

Some airlines, industry associations and fuel producers repeatedly deploy narratives to question the viability of the SAF transition. These narratives include ‘the market is not ready’, ‘SAF is too expensive’, and calling for ‘feedstock neutrality’ to dilute sustainability-based restrictions on feedstock use. Meanwhile, airlines often push SAF as a ‘silver bullet’ to resist additional regulation.

A split in perspective appears to be emerging between the aviation and oil and gas industries. Airlines emphasize scarce SAF supply as a key limitation to meeting SAF goals, while oil and gas companies frequently cite a lack of demand. The International Air Transport Association (IATA) recently accused fuel suppliers of imposing excessively high compliance fees for mandated SAF.

Considering the advocacy undertaken by CA100+ focus companies, investors would be encouraged to engage with investee companies in line with recommendations from the IPCC and the Global Standard on Responsible Climate Lobbying. This would help ensure the necessary, rapid transition of the aviation sector and the protection of carbon sinks, food security, and biodiversity in SAF policies.

The rapid growth of the aviation sector, alongside a lack of decarbonization options, makes it likely that aviation will take up an increasingly large share of Europe’s carbon budget, jeopardizing the Paris Agreement’s temperature goals. The IPCC 2022 AR6 WGIII1 report defines aviation as a “hard-to-abate” sector due to its dependency on fossil fuels, demonstrating the need for aviation to transition to non-fossil-based fuels. To enable such a transition, regions and nations have begun to legislate SAF policies–these include the EU SAF mandate (ReFuelEU), the UK SAF mandate, and the US Clean Fuel Production Credit.

Sustainable Aviation Fuel (SAF) is an umbrella term for jet fuel alternatives that reduce lifecycle greenhouse gas emissions compared to conventional jet fuel (fossil kerosene). There are two main categories of SAF, listed below:

Bio-based SAF: SAF can be produced from biological materials, including plant oils, agricultural residues, and waste. Conventional biofuels are currently widely used, but the IPCC’s AR6 WGIII report concludes that the finite availability of land and growing demands for food, feed, and fuels, exacerbated by a necessary fossil fuel phase-out, will create significant competition for land and may motivate the conversion of natural lands to crop land for biofuels. The IPCC finds that growing dedicated bioenergy crops “raises a broad set of sustainability concerns” and may be “incompatible with net-zero emissions in some contexts.”2 Consequently, safeguards are necessary to limit the impacts of bioenergy production on carbon stocks,3 alongside a scale-up of advanced biofuels.2 Additionally, an October 2025 study by Transport & Environment further revealed that due to indirect land clearance and deforestation, biofuels emit on average 16% more CO₂ emissions than the fossil fuels they replace.

Synthetic fuels (e-SAF): SAF can be produced from renewable non-biological sources, predominantly power-to-liquid (PtL) or e-fuels using renewable electricity or captured carbon dioxide. Compared to bio-SAFs, the production of synthetic fuels is in its infancy,4 but could emerge as a longer-term option which avoids the land-use constraints associated with bio-based fuels.

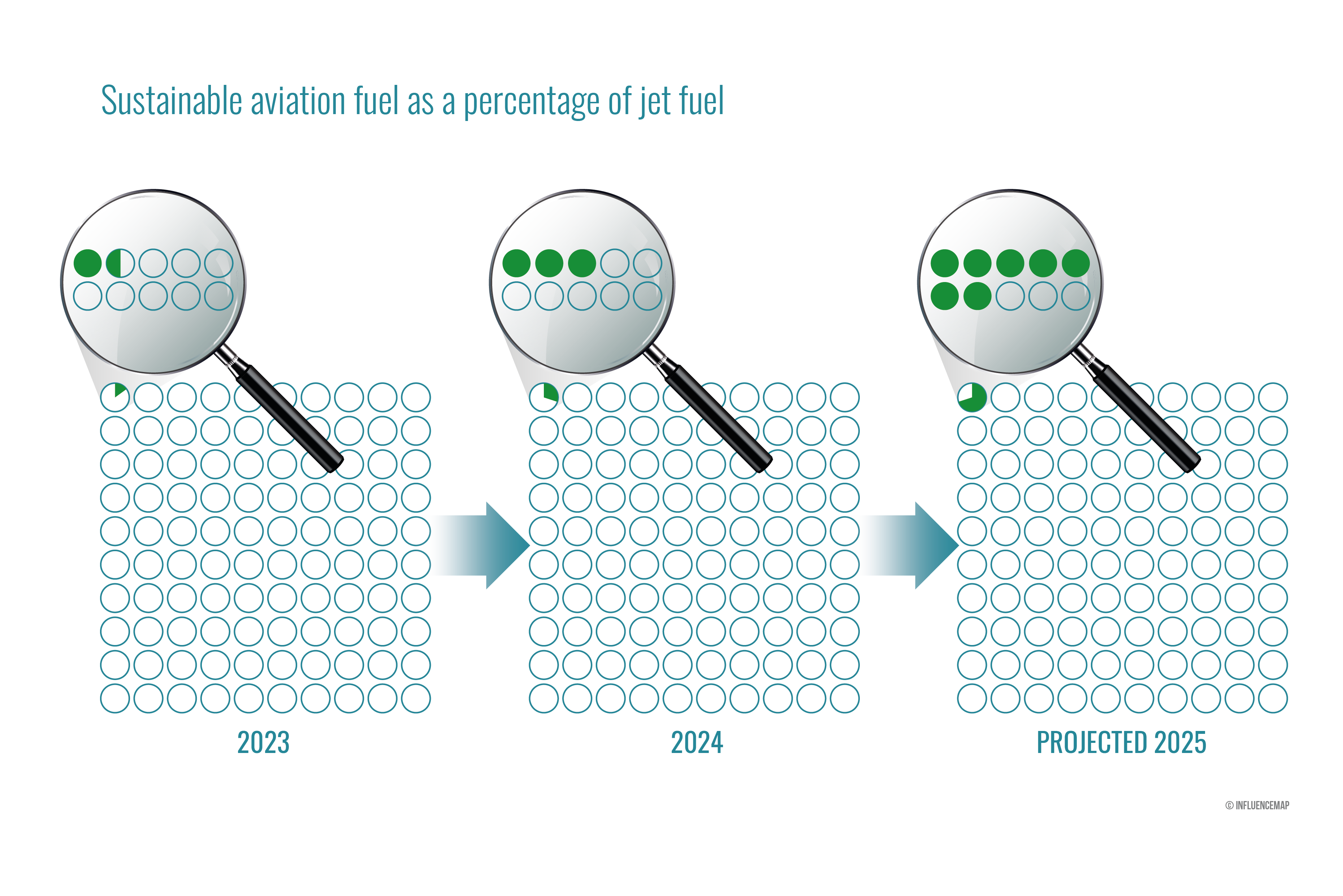

SAF production is currently lagging behind projections – despite production having doubled between 2023 and 2024, SAF accounted for just 0.3% of global jet fuel supply in 2024, and is projected to make up 0.7% in 2025. However, the International Air Transport Association (IATA) projects that jet fuel consumption will also grow, increasing from 99 billion gallons in 2024 to 103 billion gallons in 2025, resulting in approximately 985 million tons of CO₂ emissions. More recently, the term ‘sustainable aviation fuel’ has come under scrutiny; an Opportunity Green July 2025 release found that SAF is an imprecise "catch-all term" obscuring significant differences between fuel types that could mislead consumers and investors, and exposes companies to legal, regulatory and reputational risks.

Based on IPCC guidance, science-aligned advocacy on SAF feedstocks should promote SAF made from waste and residues (second generation bio-SAF), alongside e-fuels over SAF made from feedstocks that can also be used for food (first generation bio-SAF). It would urge safeguards to limit the impact of biofuels on carbon stocks, through stronger policy measures to protect carbon stores and stringent sustainability criteria that ensures direct and indirect land-use change is considered, alongside other trade-offs, such as food security and biodiversity.

Despite the IPCC's scientific warnings about the expansion of bio-based SAFs, InfluenceMap’s research has uncovered efforts by the aviation and oil and gas industries to undermine the integrity of SAFs, for example by pushing for crop-based fuels, which may contribute to global agricultural expansion, deforestation, and food displacement.

Using evidence sourced from profiles on InfluenceMap's LobbyMap database, this briefing details the direct and indirect (via industry associations) policy engagement of CA100+ focus companies in the aviation and energy sectors on SAF.

For a full list of the companies and industry associations covered in this briefing, refer to Appendix A.

This section explores corporate direct and indirect (via industry associations) engagement with key regional SAF policies in the EU, UK, and US. Overall, it finds evidence of opposition to SAF mandates and advocacy to weaken sustainability safeguards from the aviation and oil and gas industries.

To boost the supply of SAFs, EU policymakers passed the RefuelEU Aviation Initiative in September 2023. This imposes increasing mandates on fuel suppliers to include SAF in aviation fuel supplied at EU airports to all departing international flights. The regulation targets 2% in 2025, 6% in 2030, 34% in 2040, and 70% in 2050, alongside sub-targets for e-kerosene of 1.2% in 2030, rising to 35% in 2050.

To address the trade-offs associated with bio-based SAFs, ReFuelEU uses a list of sustainable feedstocks based on ‘Annex IX’ of the Renewable Energy Directive (RED), excluding food-and fuel-based crops. SAFs must meet RED’s sustainability criteria, so changes to Annex IX affect the emissions reduction potential of ReFuelEU. Annex IX has two parts: Part A covers advanced biofuels, and Part B includes used cooking oil and animal fats, which face a 1.7% cap to prevent fraud and competing uses. A complete list of Part A and B feedstocks in the December 2022 draft proposal and the March 2024 adopted directive can be found here.

Narratives around supply and cost constraints have frequently been utilized by the aviation industry in its advocacy on the EU SAF mandate:

Despite Air-France KLM broadly supporting the concept of an EU SAF mandate in a June 2025 consultation response, its CEO and Chair of Airlines for Europe (A4E), Benjamin Smith, appeared to call for a delay of the EU SAF mandate until the further maturity of the SAF market in a March 2025 Politico article.

IATA and Airlines for America (A4A) emphasized supply concerns respectively in a February 2025 position paper and April 2025 meeting with the Directorate General for Transport.

Delta and American both appeared unsupportive of the EU SAF mandate in media articles from May and February 2024.

Oil and gas companies have often focused their advocacy efforts in the EU on expanding the eligibility of feedstocks for SAF under ReFuelEU, contradicting guidance from the IPCC, which highlights the direct implications of bio-SAF production on carbon sinks, food security, and biodiversity.2

In its 2024 Climate Report published in May 2025, Shell appeared unsupportive of ReFuelEU and advocated for feedstock flexibility.

In a January 2024 Euractiv article, BP pushed for crop-based SAFs.

In a May 2024 statement, FuelsEurope advocated to expand the list of eligible biofuel feedstocks and opposed excluding certain feedstocks, such as intermediate crops, from SAF targets.

The UK SAF mandate, passed in April 2024, began in January 2025 at 2% and will rise to 10% in 2030 and 22% by 2040, with a separate power-to-liquid sub-target starting in 2028.

Used cooking oil and tallow (also known as Hydoprocessed Esters and Fatty Acids (HEFA)) is generally accepted to be the least scalable form of SAF. Across Europe, 80% of used cooking oil is imported. As key suppliers appear to export more used cooking oil than collected, fraudulent imports of mislabelled virgin oils – including palm oil – are suspected, undermining sustainability claims of used cooking oil as a fuel.

In March 2023, ahead of a consultation, UK Government proposed two options to cap the use of HEFA:5

However, following industry’s advocacy the cap was weakened in the final SAF mandate, allowing HEFA to make up 100% of SAF in 2025 and 2026, 71% in 2030, and 35% in 2040.

A ‘Revenue Certainty Mechanism’ is being developed alongside the mandate to give SAF producers a predictable price, thereby unlocking investment in the SAF market. The UK Government’s proposal stated non-HEFA projects would be granted contracts.

In December 2025, the UK government opened a consultation on crop-derived SAF under the mandate that will close in March 2026. Currently, crop-based SAF are not eligible under the mandate.

Both regional and international associations have expressed concerns about the UK SAF mandate. The following section focuses on responses to a consultation on developing the UK SAF mandate in June 2023:

Despite potentially harmful trade-offs from the large-scale production of crop-based fuels, oil and gas groups, alongside some aviation groups, pushed for crops to be eligible for SAF production under UK policy.

In June 2023 consultation responses, Airbus opposed the HEFA cap and appeared to oppose the exclusion of food-based feedstocks; Shell rejected a HEFA cap, and supported including first-generation ethanol fuels through a feedstock-neutral approach; and BP opposed the proposed HEFA cap. IATA similarly rejected a HEFA cap in a September 2024 paper.

In response to a June 2024 consultation on the Revenue Certainty Mechanism, accessed via FOI request, IATA, Boeing, and Rolls-Royce opposed the exclusion of HEFA, which risks diluting support for more advanced SAFs. In response to the same consultation, A4A also opposed the exclusion and called for a technology-neutral approach, while BP supported funding focused on advanced SAFs but appeared unsupportive of current restrictions on feedstocks under the SAF mandate.

The Clean Fuel Production Credit (45Z) is a US federal tax incentive for the production of ‘clean’ transportation fuels, including for aviation. Established under the Inflation Reduction Act (IRA) and signed into law by then-President Biden in August 2022, the credit applies to fuels with lifecycle emissions below a defined threshold. The value of the tax credit depends on the fuel’s emissions rate, which is determined by the Treasury.

45Z has been amended under the Trump administration. The budget bill, signed into law by President Trump on July 4th, 2025 – also known as the “One, Big, Beautiful Bill” – weakens the climate ambition of 45Z by removing any emissions attributed to indirect land-use change from fuel emissions calculations. Indirect land-use change occurs when corn and soybeans are used to produce fuel rather than food, requiring farmers to convert forests and natural land to cropland to replace lost food. Excluding consideration of indirect land-use change significantly weakens climate safeguards and is likely to inflate the estimated carbon savings of crop-based fuels, likely reducing the emissions reductions potential of the policy.

In the US, most advocacy on the Clean Fuel Production Credit is coordinated through two major coalitions that bring together the aviation, oil and gas, and industrial sectors, alongside their industry associations. The SAF Coalition includes A4A, American Airlines, Boeing, Shell, and United Airlines. A second group, Americans for Clean Aviation Fuels (ACAF), includes Airbus, A4A, BP, Delta Air Lines, ExxonMobil, and Rolls-Royce North America. Another example of airlines and oil and gas becoming closely aligned in the US appears to be through the Consumer Energy Alliance (CEA). Membership to this group includes A4A, Chevron, ExxonMobil, Enbridge, and Shell, and in August 2025, Delta Air Lines joined its board of directors.

Despite ACAF, A4A, and Delta supporting the policy and advocating for an extension, there was widespread support for amendments to weaken sustainability safeguards for feedstocks under the policy.

ACAF strongly supported the Trump Administration’s ‘Big Beautiful Bill’ in a July 2025 press release. This bill will inflate the estimated carbon savings of crop-based fuels by excluding the consideration of indirect land-use change emissions, incentivizing the use of corn, soy and other crops for fuel production.

In a May 2025 media article, the SAF Coalition explicitly supported amendments to weaken indirect land use change assessments under the Trump Administration’s ‘Big Beautiful Bill’, because “soybean and canola–typically higher emissions–would become more competitive for SAF compared with oils and fats”.

In December 2024 regulatory feedback, ACAF appeared unsupportive of indirect land use change in fuel emissions estimations and advocated for climate-smart agricultural practices, without stating clear conditions on monitoring, reporting, and verification protocols.

As part of their advocacy to weaken mandates and sustainability criteria for SAF, some airlines, industry groups, and fuel producers deploy narratives that question the feasibility of a SAF transition. This advocacy occurs despite the International Air Transport Association (IATA)’s public claim that SAF will deliver 65% of aviation decarbonization by 2050, or despite initiatives like Project SkyPower which bringings together CEOs from Air France-KLM, Airlines for Europe (A4E), Airbus, and Boeing to promote e-fuels.

‘The market is not ready’: A common argument employed by airlines to delay SAF mandates is that the supply of SAF is insufficient. In contrast, fuel suppliers have stressed insufficient SAF demand and limited feedstock availability.

Policy and feedstock ‘neutrality’: For many years, narratives concerning ‘policy neutrality’ have been deployed by the oil and gas industry to oppose or dilute technology-specific policy aimed at decarbonization, instead often promoting fossil-based solutions and weak government intervention. In recent policy discussions, ‘feedstock neutrality’ appears to have been likewise adopted as a narrative to advocate against restrictions on SAF feedstocks, which are designed to safeguard against the significant sustainability risks associated with crop-based feedstocks. Concerns around insufficient feedstocks are often used to justify why a policy neutral approach is needed, accompanied by calls to broaden the feedstock base.

SAF is ‘too expensive’: The IPCC estimates that bio-SAF is likely to cost around three times more than fossil kerosene, while the cost of e-SAF is estimated at four to six times higher.4 Policy instruments to reduce this gap include the EU Sustainable Transport Investment Plan (STIP) and the EU ETS SAF allowances. Notably, fossil kerosene remains exempt from taxation under the EU’s Energy Taxation Directive (ETD). Some aviation groups are pointing to fuel suppliers for exacerbating the higher costs of SAF.

SAF is a ‘silver bullet’: Despite arguments regarding SAF costs, supply, and feedstocks, some aviation actors suggest that broader regulation is unnecessary as SAF will facilitate the sector’s decarbonization. A 2022 study by Possible found that all but one of 50 voluntary climate targets set by the international aviation industry were missed, abandoned, or forgotten. IATA itself failed to meet the four global SAF targets it had set in 2007 (10% by 2017), 2011 (6% by 2020), 2012 (4.5% by 2020), and 2014 (3% by 2020), with each target becoming progressively weaker over time. These failures call into question the integrity of aviation's voluntary commitment to SAF.

As advocacy to weaken and/or obstruct SAF mandates, policies, and safeguards on feedstocks continues, additional steps are required by investors globally to ensure the necessary, rapid transition of the aviation sector and the protection of carbon sinks, food security, and biodiversity. In line with guidance from the IPCC and the Global Standard on Responsible Climate Lobbying, investors are encouraged to prioritize the following asks and actions:

Encourage science-aligned positions on SAF feedstocks

Promote supportive policy frameworks

Leverage coalitions and alliances

In aid of this, InfluenceMap’s Recommended Investor Asks provides a concise guide to engagement with companies in line with the recommendations outlined in the Global Standard on Responsible Climate Lobbying. Other resources to support investors that are offered by InfluenceMap include detailed 1-2-1 company calls and briefings and detailed investor notes to aid voting decisions on shareholder and management resolutions.

| Industry Associations | Membership to IATA | Membership to A4E | Membership to A4A | Membership to FuelsEurope | Membership to AirlinesUK | |

|---|---|---|---|---|---|---|

| Companies | InfluenceMap Performance Band (Global) | D+ | C- | D- | D | C- |

| Air France-KLM | C- | Member | Yes | Yes | ||

| American Airlines Group | D+ | Member | Yes | |||

| Delta Air Lines | D | Member | Yes | |||

| Qantas | C | Member | ||||

| United Airlines | D | Member | Yes | |||

| Airbus | C | Strategic partner | Yes | |||

| Boeing | D+ | Strategic partner | Yes | Yes | ||

| Rolls-Royce | C- | Strategic partner | Yes | |||

| BP | C- | Strategic partner | Yes | |||

| Eni | D+ | Strategic partner | Yes | |||

| ExxonMobil | D | Strategic partner | Yes | |||

| OMV | D+ | Strategic partner | Yes | |||

| Phillips 66 | C+ | Strategic partner | Yes | |||

| Repsol | D+ | Strategic partner | Yes | |||

| Shell | C- | Strategic partner | Yes | |||

| Siemens Energy | C- | Strategic partner |

1 IPCC AR6 WGIII, Chapter 10, Section 10.5.1

2 IPCC AR6 WGIII, Chapter 6, Section 6.4.2.6

3 IPCC AR6 WGIII, Chapter 7, Section 7.6.3

4 IPCC AR6 WGIII, Chapter 10, Section 10.5.3

5 Pathway to net zero aviation: Developing the UK sustainable aviation fuel mandate A second consultation on reducing the greenhouse gas emissions of aviation fuel in the UK, Page 34.