New analysis from InfluenceMap finds that global insurance groups have mobilized to slow down efforts by supervisors and regulators to tackle climate-related insurance risk. In responses to four consultations conducted by the global standard setter for insurance regulators and supervisors—the International Association of Insurance Supervisors (IAIS)—a number of industry associations attempted to downplay the risk that climate change poses to the insurance sector, while opposing the need for additional supervisory action.

The research finds that industry groups questioned the climate risk implications for the insurance sector, asserted that insurers have proven they can sufficiently manage climate risks, and posited that natural catastrophe events are not frequent enough to require additional guidance or regulation. However, as natural catastrophes and extreme weather events increase in frequency and severity, so does climate-related risk—impacting policyholder property and assets, insurers’ operations and investments, and overall financial stability.

A number of respondents argued that IAIS guidance is too “prescriptive,” and some argued that insurance supervisors lack any mandate to promote the transformation to a climate-neutral environment. Some groups advocated for increased government action on disaster prevention and mitigation as an alternative to the proposed standards, arguing that this effort falls into the remit of "real economy" policymakers. Despite these arguments, InfluenceMap did not find evidence of industry groups advocating for ambitious government policy to support the climate transition.

This briefing examines the global insurance industry’s attempt to shape climate-related insurance supervisory guidance being developed by the International Association of Insurance Supervisors (IAIS). Building upon InfluenceMap’s November 2023 briefing which examined engagement from October 2020 to March 2023, this update analyzes more recent consultations and industry responses.

The International Association of Insurance Supervisors (IAIS) is an international voluntary organization of insurance supervisors and regulators. Members cumulatively oversee 97% of the world’s insurance premiums and include the US National Association of Insurance Commissioners (NAIC), the UK Prudential Regulation Authority (PRA), the Japanese Financial Services Agency (FSA), and the European Insurance and Occupational Pensions Authority (EIOPA). IAIS is responsible for establishing principles and standards for the supervision of the insurance sector and providing guidance to assist with their implementation.

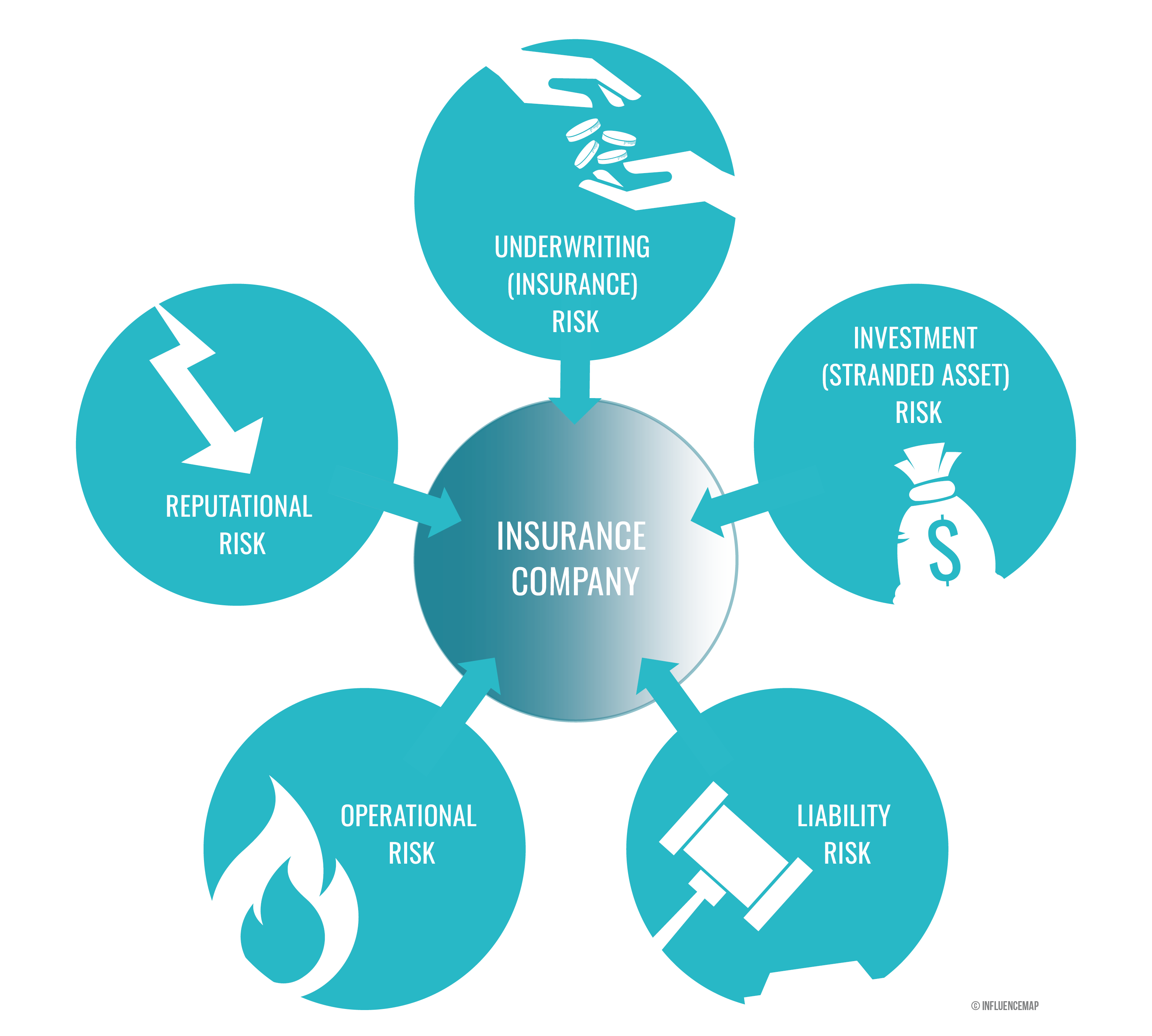

As disaster costs continue to rise globally, insurers are increasingly vulnerable to climate risk. As seen in Figure 2, alongside physical and transition risk, insurers are subject to several climate-related prudential risks including litigation risk, liquidity risk, and underwriting risk. Accordingly, it is critical that both insurers and supervisors adequately understand and manage climate risk.

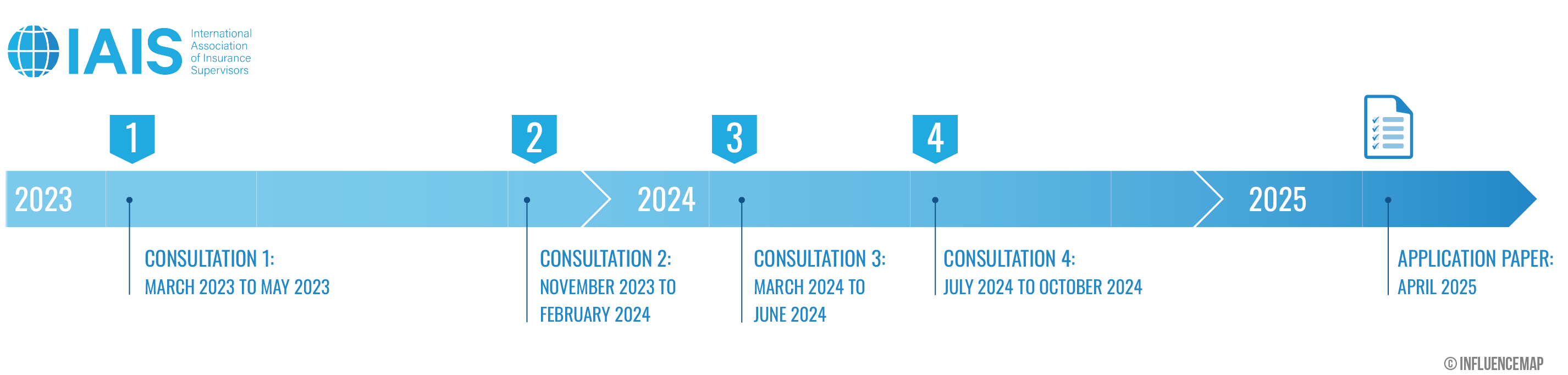

The IAIS has identified climate risk as a strategic theme, and throughout 2023 and 2024, the body ran four climate risk-related public consultations. The consultations sought feedback on proposed changes to certain Insurance Core Principles (ICPs)—a globally accepted framework for insurance supervision, consisting of Principle Statements, Standards, and Guidance—and on new supporting material for insurance supervisors to better incorporate climate risk into supervision of the insurance sector. As these guidance papers are likely to inform insurance supervision across jurisdictions, InfluenceMap has tracked and analyzed industry associations’ responses to these consultations.

The first IAIS climate risk consultation, which ran from March to May 2023, proposed explicitly naming climate risk within the global framework for insurance supervision. The consultation set out to assess whether necessary to make changes to existing material related to corporate governance and risk management and internal controls, and to seek feedback on its overall climate-related supervisory guidance work. InfluenceMap’s 2023 briefing assessed initial responses to this consultation, but the IAIS had not yet released its full list of consultation responses upon publication.

The second consultation, which ran from November 2023 to February 2024, was twofold. The first paper focused on climate risk market conduct issues in the insurance sector, specifically greenwashing around insurers’ operations and products. The second paper considered the use of climate-related scenario analysis as a supervisory tool.

The third consultation, which ran from March to June 2024, proposed additions to guidance for climate-related aspects of investments and enterprise risk management for solvency purposes. It discussed corporate governance, risk management and internal controls, valuation of assets and liabilities for solvency purposes, and insurers’ investments.

The final round of consultations, which ran from July to October 2024, was split into two draft application papers. One paper focused on supervisory reporting and public disclosure regimes, while the other paper covered macroprudential supervision and group-wide supervision.

The consultations culminated in an IAIS April 2025 Application Paper on the supervision of climate-related risks in the insurance sector. The application paper generally reflects the proposed drafts and aims to support insurance supervisors in assessing climate-related risks and provide guidance on how best to integrate those risks into supervisory frameworks. Suggestions include supervisory oversight of corporate governance and board knowledge of climate risk, and methods for insurers to consider climate when assessing existing risk categories. IAIS also proposed that supervisors consider the potential impact of climate change on insurers’ investments and require insurers to effectively disclose climate-related risks and conduct forward-looking scenario analysis.

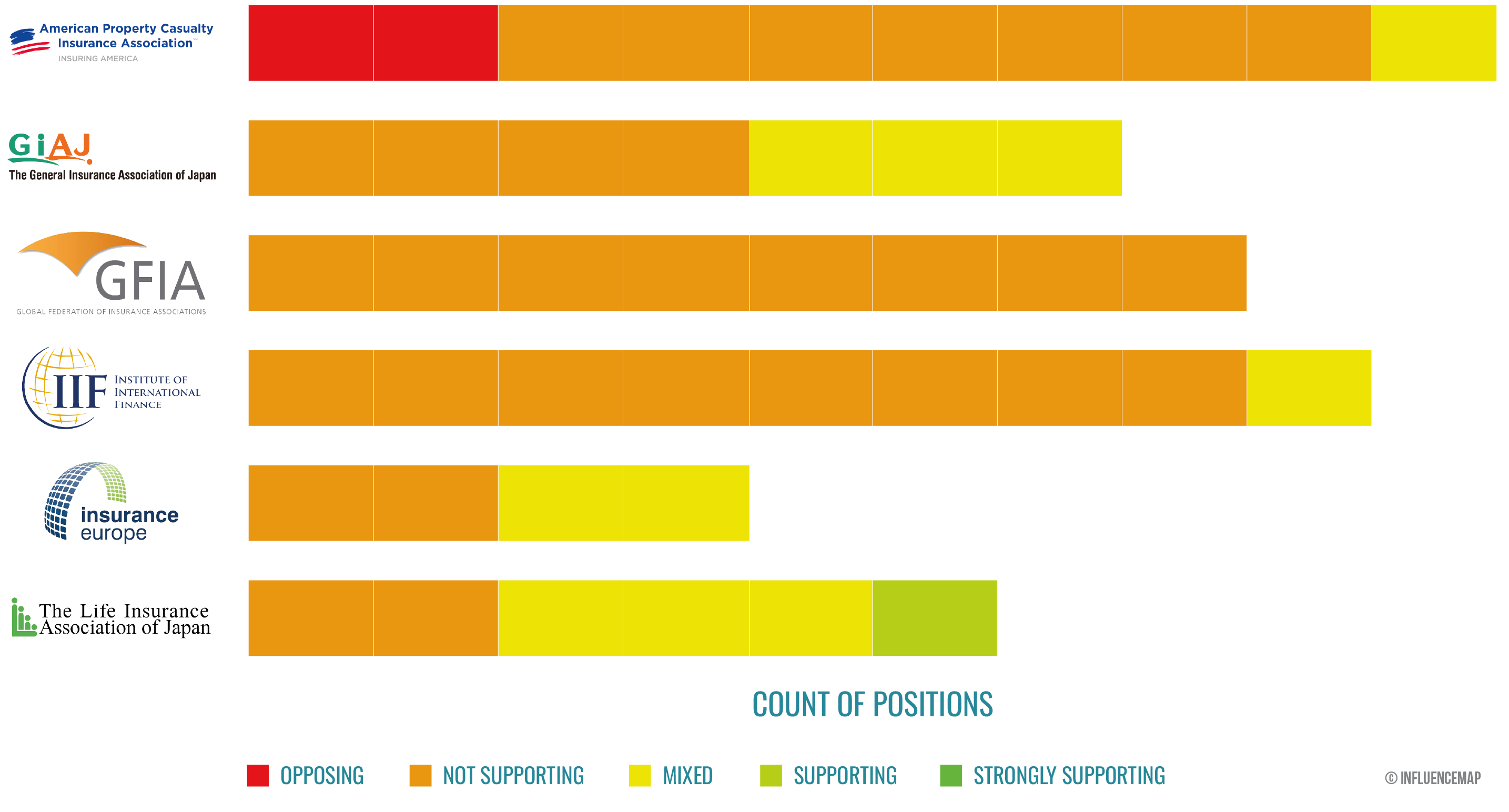

This briefing focuses on responses from some of the largest insurance industry associations and trade groups to these consultations across a number of regions: the American Property Casualty Insurance Association (APCIA), the National Association of Mutual Insurance Companies (NAMIC), the Institute of International Finance (IIF), the Global Federation of Insurance Associations (GFIA), the Life Insurance Association of Japan (LIAJ), Insurance Europe, the General Insurance Association of Japan (GIAJ), and the US Chamber of Commerce1. Of these respondents, only the LIAJ took supportive positions on the proposed guidance. All other groups showed either mixed support or, in most cases, downplayed the systemic risk climate change poses to the insurance industry and suggested that additional regulation is unnecessary.

1 Detailed membership information of the most engaged insurance industry associations can be found in the appendix.

Throughout their responses to the IAIS, insurance industry associations continued to downplay the systemic and urgent nature of the climate-induced insurance crisis.

As previously assessed by InfluenceMap, a number of industry associations including the US Chamber, IIF, NAMIC, and APCIA appeared to question the assertion that climate risks are a threat to financial stability.

In its response to the first consultation, the Chamber stated that “we question the implication that climate change is currently a financial stability risk to the insurance sector.”

By contrast, LIAJ did acknowledge the “possible risk” of climate change on financial stability, and as such supported the climate risk work of the IAIS as “beneficial to the insurance sector.”

While GIAJ appeared to accept the impact of climate change on the insurance industry, it argued that climate change is not relevant for asset-liability management.

IIF and Insurance Europe questioned the materiality of climate risks for the insurance industry.

IIF stated that “The Draft Application Paper implies that climate-related risks are material to all insurers. [...] We do not agree with this inference.”

GFIA asserted that “As far as managing catastrophe risk, property/casualty insurers have proven they are capable and up to the task of managing this risk.”

The Senate Budget Committee has pointed to a 2023 Economic Report of the President that warns that “property insurance against catastrophic natural hazards is at the forefront of climate change risk exposure and is already showing signs of strain.”2

Industry groups’ positioning appears to be misaligned with the positions of some of their members, which have acknowledged the impact of the climate crisis both explicitly, and in their actions.

A recent statement from Allianz board member Günther Thallinger characterized the insurance crisis as on track to destroy capitalism, and warned that it will not be a “one-off market adjustment.” Describing climate change as a “systemic risk that threatens the very foundation of the financial sector,” Thallinger stated that “if insurance is no longer available, other financial services become unavailable too. A house that cannot be insured cannot be mortgaged. [...]. This is a climate-induced credit crunch.” Reinsurer Swiss Re argues that “climate change poses one of the most pervasive risks to our planet and our prosperity. Its effects are already evident and shaking up our risk landscape.”

Insurers’ tacit acknowledgement of this crisis can be seen from more expensive premiums, increased policy non-renewal rates, emergency rate increases, and a higher number of non- or under-insured properties.

In the US, home insurance costs increased by an average of 24 percent from 2021 to 2024, and rose to an all time-high in the first half of 2025. Furthermore, it is estimated that 67% of US homeowners are underinsured. In the wake of the 2025 Los Angeles wildfires, State Farm sought and received “urgent assistance in the form of emergency interim approval of additional rate to help avert a dire situation for our customers and the insurance market in the state of California.” Citing rising home replacement costs and more frequent severe weather events, State Farm claims that for every $1 it earned in Illinois in 2024, it paid out $1.26. As noted in the appendix below, Allianz holds board positions of IIF and Insurance Europe, as does Swiss Re, which also appears to be a board member of APCIA.

Figure 4 displays the distribution of industry group’ positioning toward various tools, oversight, and guidance proposed by the IAIS throughout the four consultations. The majority of positions fall into the “not supporting” category, with GFIA and IIF each weighing in with eight instances of unsupportive comments across the four consultations. The following sections describe the climate risk-related tools that the IAIS has proposed, and the selected industry groups’ responses to these proposals.

The IAIS suggested the use of scenario analyses as a tool to inform further supervisory or policy outcomes and to define the resilience of insurers’ business strategy. It also proposed the use of scenario analysis as an input to insurers’ Own Risk and Solvency Assessments (ORSAs), and as a tool to inform insurers’ investment policies and asset-liability management policies.

LIAJ (Japan) and GIAJ (Japan) supported supervisors encouraging some use of climate-related scenario analysis exercises, while cautioning against mandated disclosure of the results of these exercises due to data unavailability and uncertainty.

APCIA (US), IIF (Global), GFIA (Global) and Insurance Europe (Europe) warned against overreliance on scenario analysis and argued against its effectiveness.

Responses to the second consultation on market conduct focused particularly on the Natural Catastrophe section of the draft, asserting that it was too prescriptive. Some groups argued for increased government action on disaster prevention and mitigation as an alternative to the proposed standards and downplayed the frequency of natural catastrophes.

The IAIS draft on climate risk market conduct issues recommended that supervisors develop a definition of greenwashing, define a benchmark for measuring the level of environmental benefit of a product, and ensure that the label of “sustainable” for insurance products be used in a fair and not misleading way. To achieve this, the IAIS suggested that supervisors could monitor product design, delivering, marketing, and performance, and could encourage insurers to report their progress in meeting sustainability commitments. IAIS also suggested that "without undue influence” in pricing practices, supervisors should require the pricing of natural catastrophe (NatCat) products to reflect adequate actuarial models, including “the increasing frequency and intensity of NatCat events.”

APCIA stated that “Overall, this section fails to recognize that nat cat protection gaps are the result of society-wide failure to pursue resilience and economic conditions that are not created by insurers. Only society-wide actions, with help from insurers in cooperation with supervisors, can close those gaps.” Comments from GIAJ, GFIA and IIF echoed this point, calling out the need for government action on disaster prevention and mitigation. In response, the IAIS noted that “this application paper is aimed at insurers, not at the general public.”

GFIA stated in its response that “Insurers fully understand the challenges posed by climate risk and are working cooperatively with supervisors around the world to disclose relevant information, provide useful coverage and, even more importantly, to assist societies to become more resilient by mitigating and adapting to their climate risk.” Later, in its response, GFIA questioned that the frequency of NatCat events necessitates a change in insurers’ business models, stating that “these events occur reasonably rarely, so it would be a waste of resources to scale up permanently waiting for the next one to occur.”

In 2024 there were 27 confirmed weather/climate disaster events with losses exceeding $1 billion each in the United States alone. The US annual average number of billion dollar events (CPI adjusted) for the last five years (2020-2024) is 23 events, over a 2.5 times increase from the US national average of 9 events for the period 1980–2024. Bloomberg reports that in a 12-month period ending 1 May 2025, the US has spent nearly $1 trillion dollars on disaster recovery and other climate-related needs. In the first six months of 2025, total US economic losses from natural catastrophe accounted to $126 billion, the costliest first half of a year on record for the US.

APCIA and GFIA also argued that greenwashing is not a pressing issue for insurance products.

Policymakers, however, have recognized greenwashing as an issue in the insurance product space. In June 2024 the European Insurance and Occupational Pensions Authority (EIOPA) released a report that stated “A lack of standards in relation to non-life products with sustainability features can lead to a higher risk of greenwashing,” and concluded that “Despite POG [Product Oversight and Governance] being a well-established concept in the insurance regulatory landscape, the integration of sustainability-related objectives in the POG process is not adequate, especially for non-life products.”

Generally, industry groups did not support the proposals in the third consultation on climate risk supervisory guidance, with LIAJ, APCIA, IIF, GFIA and Insurance Europe cautioning against elevating climate risk above other risks. All examined respondents did not support the incorporation of climate factors into investment activities, and APCIA, IIF, GFIA and Insurance Europe did not support explicitly linking remuneration with achieving climate goals.

In this consultation, the IAIS suggested that supervisors should require insurers to consider the potential effects of climate change in their investments through traditional risk categories, as well as consider how investment decisions could negatively impact climate change. IAIS suggested that insurers, after considering these risks, could decide to take steps such as engaging with investee companies, divesting of certain assets, or changing their investment strategy.

While Insurance Europe merely described this as “quite prescriptive,” GFIA disagreed with the IAIS statement that “insurers with significant investment exposures to assets that are vulnerable to climate-related risks are potentially more exposed to systemic risk,” arguing that “It is unclear why this is characterised as “systemic risk” [...] Moreover, it would seem appropriate for insurance supervisors to be equally cautious about concentrations in “green” investments.”

Respondents questioned the mandate of supervisors to regulate climate risks. APCIA argued that some of the proposed changes “imply that insurance supervisors should act as societal policymakers, and that is neither their role nor within their authority.” This was echoed in the responses of Insurance Europe and GFIA, which both stated that “it is not within the mandate of insurance supervisors to promote the transformation to a climate-neutral environment. In addition, the supposed emphasis on climate-related goals may expose senior management and the board to conflicts of interest.”

LIAJ, APCIA, IIF and GFIA argued that current supervisory measures are sufficient, and that climate risk is well-managed. This consultation proposed the use of scenario analysis as a macroprudential tool and other supervisory measures, including specific interventions to prohibit an insurer from underwriting certain risks or applying a climate-related capital add-on.

GFIA emphasized “the crucial role insurers play in managing risks on behalf of the broader economy, thereby mitigating overall systemic risk.” Furthermore, GFIA stated that “climate risk also presents an opportunity for insurers, given that risk management is their core business.”

The IIF again appeared to question the relevance of climate risk to the insurance industry: “The IAIS should describe in sufficient detail the evidence supporting a finding that there are substantive implications from climate change for the insurance sector.”

In contrast, US Senate Budget Committee stated in its December 2024 report—“Next To Fall: The Climate-Driven Insurance Crisis Is Here – And Getting Worse”—that “unless the United States and the world rapidly transition to clean energy, climate-related extreme weather events will become both more frequent and more violent, resulting in ever-scarcer insurance and ever-higher premiums,” and warned of “a collapse in property values with the potential to trigger a full-scale financial crisis similar to what occurred in 2008.” The Economist reported that estimates suggest that “climate change and the fight against it could wipe out 9% of the value of the world’s housing by 2050—which amounts to $25trn, not much less than America’s annual GDP. It is a huge bill hanging over people’s lives and the global financial system.”

IIF also suggested that supervisory action could lead to a withdrawal or reduction in insurance coverage, arguing that “prohibiting an insurer from underwriting certain climate-related risks or withholding approval for acquisitions may have negative impacts on insurance markets and policyholders and may run counter to the need to maintain or improve access to coverage.”

While Insurance Europe supported the incorporation of climate factors into the prudential regulation—“Insurance Europe agrees that potential financial stability implications of climate-related risks should be an integral part of macroprudential monitoring, and therefore the IAIS’s efforts to provide supporting material for national insurance supervisors are welcomed”—the group, along with APCIA, LIAJ, GFIA and the IIF did not support the proposed suggestion of a capital add-on as a risk management tool. In November 2024, the European Insurance and Occupational Pensions Authority (EIOPA) recommended additional capital requirements for fossil fuel assets on European insurers’ balance sheets in order to “better align capital requirements with insurers' actual risk exposures.”

The following table overviews member details of the most engaged insurance industry associations, where available.

| Color | Membership Status |

|---|---|

| Senior executive holds role on the association’s board or executive committee, or insurer is a member of climate change/environmental committee or working group | |

Insurer holds membership to association | |

Insurer is not a member of this association |

| Insurer | APCIA | IIF | Insurance Europe | GIAJ | LIAJ |

|---|---|---|---|---|---|

| AXA | |||||

| Allianz | |||||

| American International Group (AIG) | |||||

| Berkshire Hathaway | |||||

| Chubb | |||||

| Cigna | |||||

| Dai-ichi Life Holdings | |||||

| Generali | |||||

| Liberty Mutual | |||||

| Manulife | |||||

| MAPFRE | |||||

| Massachusetts Mutual Life Insurance Company | |||||

| Meiji Yasuda Life Insurance | |||||

| MetLife | |||||

| Munich Re | |||||

| Nationwide | |||||

| Nippon Life Insurance | |||||

| Northwestern Mutual | |||||

| Ping An Group | |||||

| Prudential | |||||

| Prudential Financial | |||||

| ORIX Group | |||||

| Swiss Re | |||||

| Talanx | |||||

| TIAA | |||||

| The Hartford | |||||

| Travelers | |||||

| Unipol | |||||

| Zurich Insurance |

3 GFIA's membership is made up of regional and national insurance associations, including APCIA and Insurance Europe, so its membership is not listed in this table. Membership to Insurance Europe is often indirect, via national associations, and thus only board/committee membership is listed. APCIA does not disclose membership, so only board membership as of April 2025 is listed.