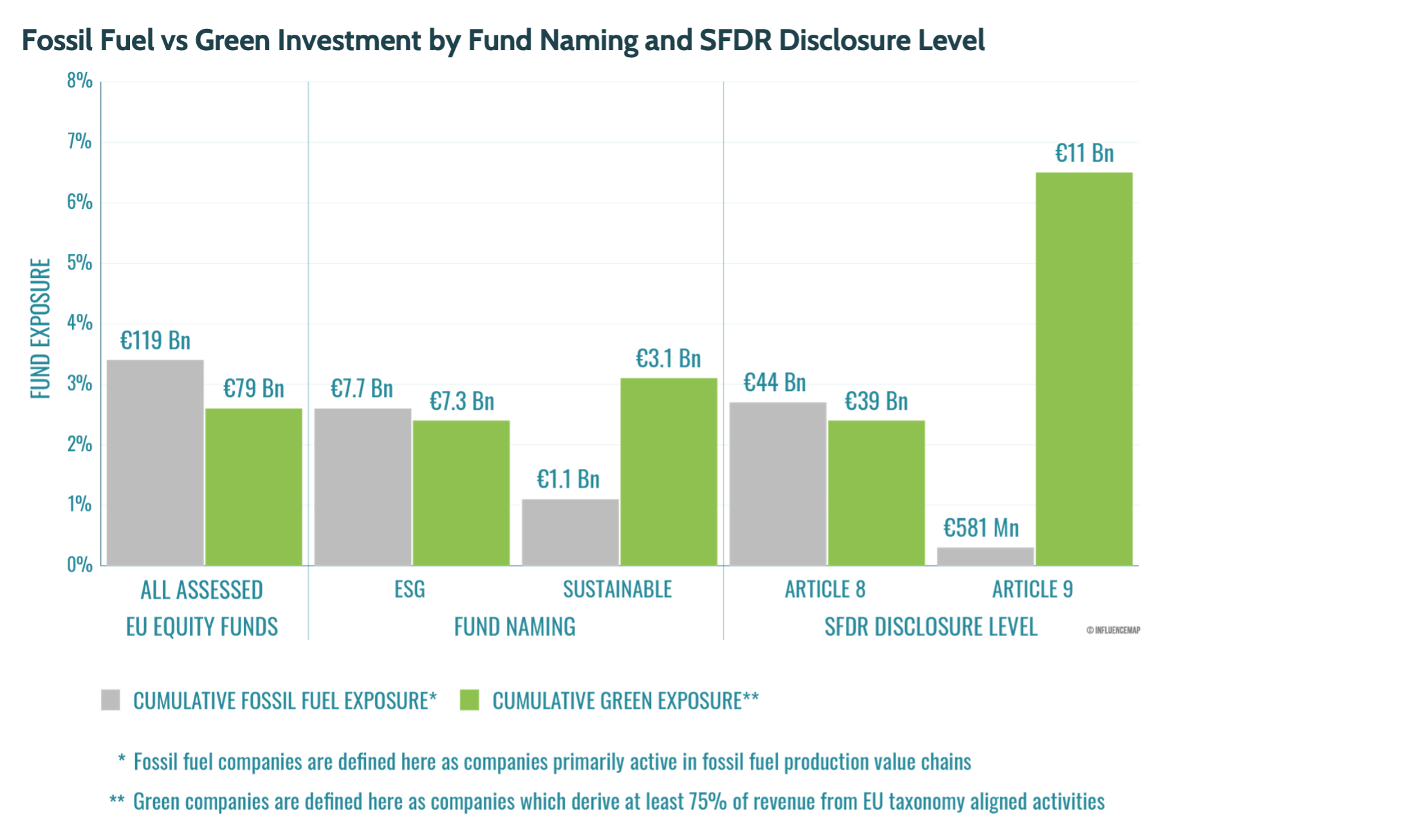

New analysis by InfluenceMap of the European fund market shows that a third of funds using ESG or climate- related terminology in their names are more invested in fossil fuel companies than green companies. The report also reveals inconsistencies between funds’ use of climate-related names and their level of disclosure under the Sustainable Finance Disclosure Regulation (SFDR) (1). For example, 60% of funds identified as using climate-related terms in their name do not disclose under SFDR Article 9, the category designated for funds with a primary sustainability objective.

Recently, the European fund market has seen a significant increase in interest in ‘sustainable’ investing, providing a strong incentive for funds to use ESG and climate-related terminology in their names. In parallel, regulators have become increasingly concerned about the consistency and transparency of funds using these terms and have introduced regulation to limit the risk of greenwashing.

The findings of the report suggest that so far SFDR has not achieved its aim of limiting greenwashing in this market. The widespread misalignment identified between the climate performance of funds and the climate- commitments implied by their names is particularly concerning given that fund names are central to the proposed categorization system for the new ESMA regulations (2). There appears to be a significant amount of work needed if funds are to meet ESMA’s criteria by the time this regulation comes into force in May 2025.

These findings are the result of analysis by InfluenceMap’s FinanceMap platform of the climate performance of European equity funds, based on three metrics: fossil fuel investment, green investment, and net zero alignment (3). In this analysis, fossil fuel companies are defined as companies primarily active in fossil fuel production value chains, while green companies are defined as those which derive at least 75% of revenue from EU taxonomy aligned activities.

Key findings:

Tom Alcoran, Senior Analyst at InfluenceMap said: **

“Thousands of funds are representing themselves as climate positive, either by using climate-related names or by disclosing under SFDR Article 8 or Article 9, despite their underlying investments painting a very different picture. This shows that the lack of consistency and transparency which has been a feature of sustainable funds over the past years continues to persist in the EU fund market. Without funds changing their portfolio allocation or rebranding to meet ESMA’s incoming fund naming criteria, many risk non-compliance.”

Click here for full report and graphics

Kitty Hatchley, Press Officer, InfluenceMap (London)

Email: kitty.hatchley {@} influencemap.org